FILE 08: RUNE TECHNOLOGIES

One Code. $876M Market. 89% Civilian Dominated. Time to Strike.

This Week's 60-Second Snapshot

Company: RUNE Technologies – AI-enabled predictive logistics replacing Excel spreadsheets and whiteboards in contested military operations

Anchor Code: PSC D302 – IT and Telecom Systems Development ($876.74M in FY24-25 DoD obligations per USAspending.gov)

Method: Analyzed publicly available contract data + active opportunities + FY26 defense budget documents

Opportunities Uncovered: 4 active opportunities aligning with AI-driven logistics (verified active on SAM.gov as of July 31, 2025), multiple FY26 budget programs showing increased contested logistics funding

Primary takeaway: PSC D302 reveals a fragmented market with GSA dominating at $221.73M but DoD representing only $98.78M—creating white space for defense-focused vendors to capture underserved military requirements

Who This Analysis Serves:

📍 Early-stage founders: Your federal roadmap starts here

📍 Defense investors: Portfolio-wide intelligence in one place

Choose your depth - skim for insights or dive deep for execution

Each week, I select one VC-backed defense startup paired with one NAICS code/PSC and dive deep into their primary market using public budget data and procurement signals. The goal? To reveal the hidden pathways to federal contracts that most companies miss.

Important note: While I use RUNE Technologies as this week's example, I'm demonstrating how I would approach their federal market strategy using PSC D302 as a foundation—not prescribing what RUNE should do or hasn't already figured out internally. Many exceptional defense startups have sophisticated federal strategies; others are still navigating these complex waters. My goal is to present hard data in a transparent, systematic way that helps any startup—regardless of their current federal expertise—see alternative perspectives on market entry. Think of this as one analyst's framework applied to real companies for illustrative purposes.

Framing the situation: a federal IT market so fragmented that civilian agencies dominate while defense-specific requirements go underserved. While that might sound like bad news for a military-focused startup, it's actually a massive opportunity—especially for a company promising AI-driven logistics that works "in five minutes what would have taken three weeks" in contested environments where traditional cloud-based systems fail.

RUNE Technologies emerged from stealth earlier this year as ex-Anduril executives' answer to military logistics chaos, targeting a market where todays systems are often analog and warfighters lack basic supply chain visibility. While RUNE specifically targets contested logistics operations, they'll compete within the broader PSC D302 IT systems development market—an $876.74M landscape where defense represents only 11% despite massive modernization needs. The company's radical approach—edge-first AI that operates on 5kbps connectivity.

This week, I'm demonstrating how RUNE could navigate from their $30M+ in funding (seed + Series A) to DoD contracts, using PSC D302 as our lens into the federal IT procurement ecosystem where military requirements remain vastly underserved.

Let's decode the opportunity.

0️⃣ Market Research Phase

Anchor Code: PSC D302 – IT and Telecom Systems Development: My deep dive into PSC D302 contracts (per USAspending.gov FY24-25 data) exposed a market dominated by civilian agencies but underserved in defense-specific requirements. This isn't just opportunity—it's validation that DoD needs purpose-built solutions for contested environments where traditional IT approaches fail.

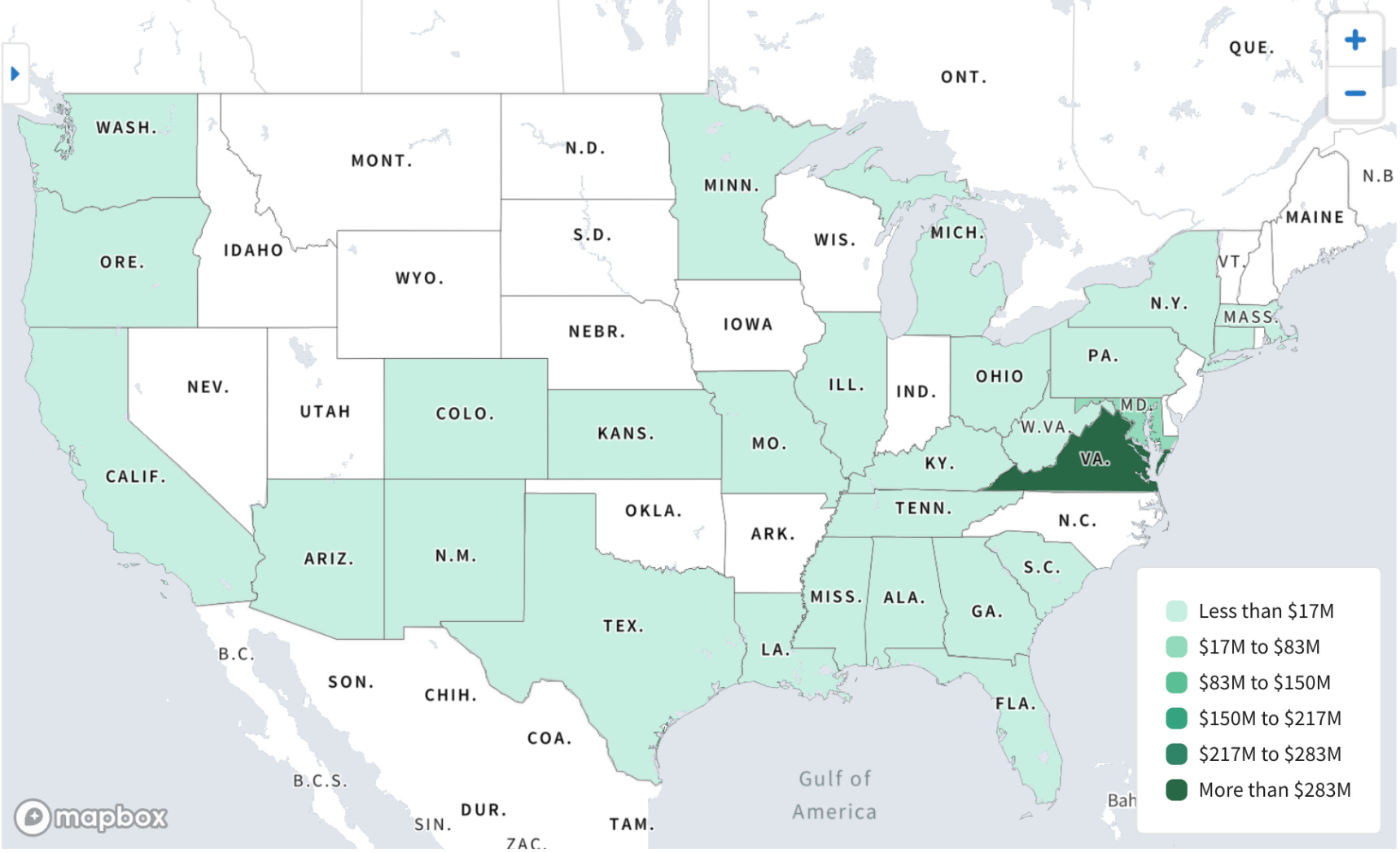

Geographic Concentration Reveals Strategic Entry Points

Location Patterns Expose Where Defense IT Dollars Aren't Flowing—Yet

The concentration reveals entrenched relationships around civilian agencies, but notice the lighter shading in traditional defense technology corridors—San Diego, Huntsville, Colorado Springs. For RUNE, this geographic white space represents opportunity to capture defense-specific requirements underserved by Beltway incumbents.

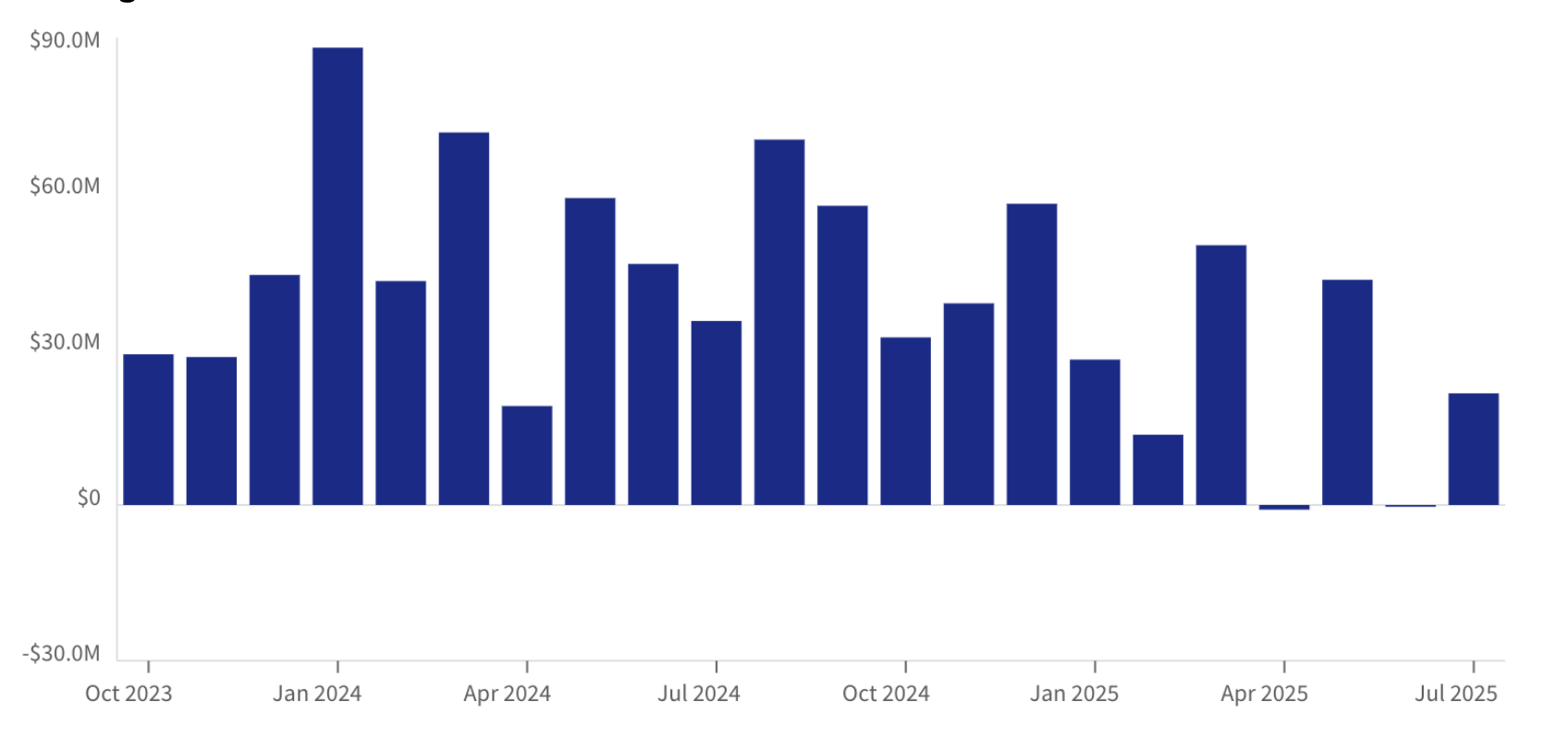

Monthly Obligation Patterns Expose Funding Cycles

Federal money follows predictable rhythms. Master these patterns, and you'll know when to strike:

These erratic spending patterns reveal opportunity—while traditional defense contractors cluster around Q4 surges, PSC D302's volatile month-to-month swings indicate fragmented buying across multiple agencies. This unpredictability rewards agile companies like RUNE that can respond quickly to sudden procurement opportunities rather than waiting for annual cycles.

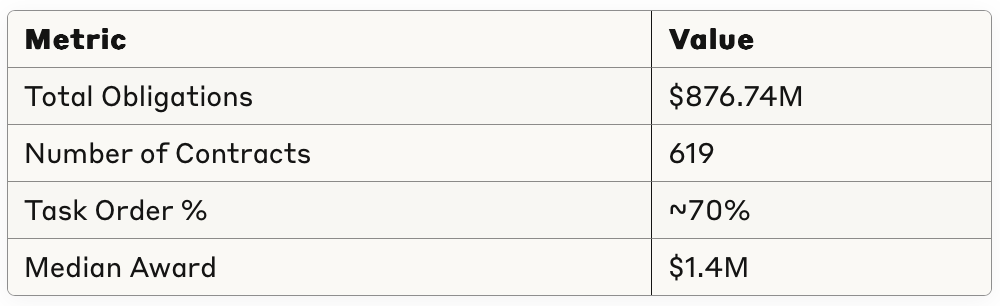

Key Market Metrics (Source: USAspending.gov FY24-25):

The market structure reveals heavy reliance on existing contract vehicles with ~70% flowing through task orders. But here's the insight: civilian-focused vehicles dominate, creating gaps for defense-specific solutions that can't be delivered through GSA schedules.

Why This Matters: PSC D302's market structure reveals a fundamental mismatch—civilian agencies drive 89% of spending while defense-specific requirements go unmet. The erratic monthly spending patterns and geographic concentration in traditional government corridors create openings for companies willing to think differently about federal IT. For RUNE, this is validation that the DoD desperately needs purpose-built solutions for contested environments where civilian IT approaches fail.

Ways to Leverage This:

Geographic Arbitrage - Establish presence in underserved defense tech hubs (Huntsville, Colorado Springs) rather than competing in saturated Northern Virginia

Timing Strategy - Target the volatile spending months rather than traditional Q4, when competition is less predictable

Vehicle Innovation - Create new defense-specific contract vehicles rather than forcing military requirements through civilian GSA schedules

Market Positioning - Message explicitly as "built for contested operations" to differentiate from civilian IT vendors who dominate current spending

1️⃣ Actionable Defense Roadmap

From Ex-Anduril Innovation to DoD Contracts: RUNE Technologies stands at a critical juncture—venture-backed logistics innovation meeting urgent military modernization needs. Their radical approach—AI-driven predictive logistics that works when communications fail. But superior technology alone won't win federal contracts. Here's how a company like RUNE could navigate this market:

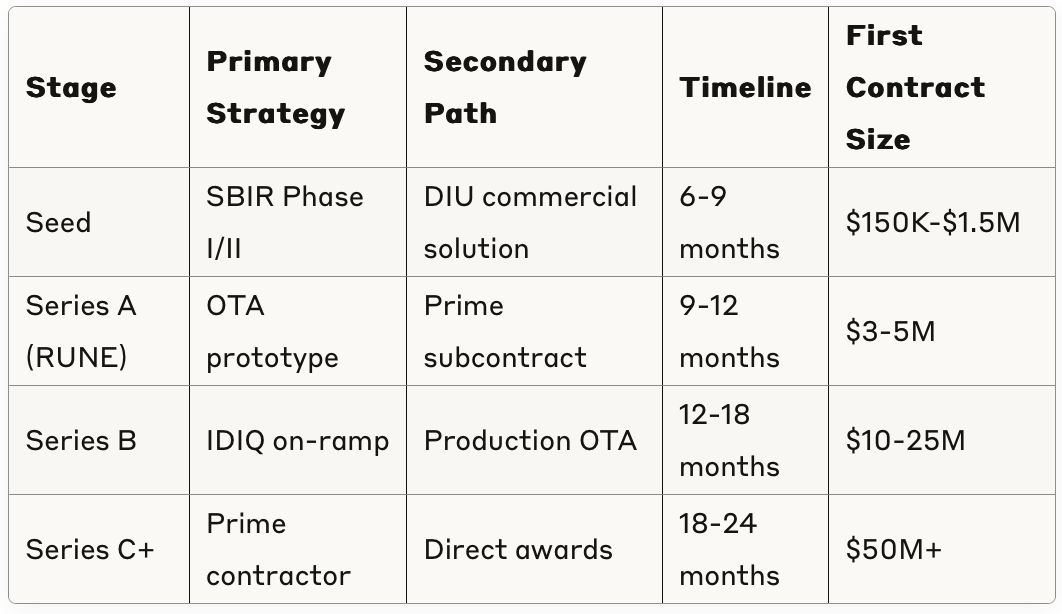

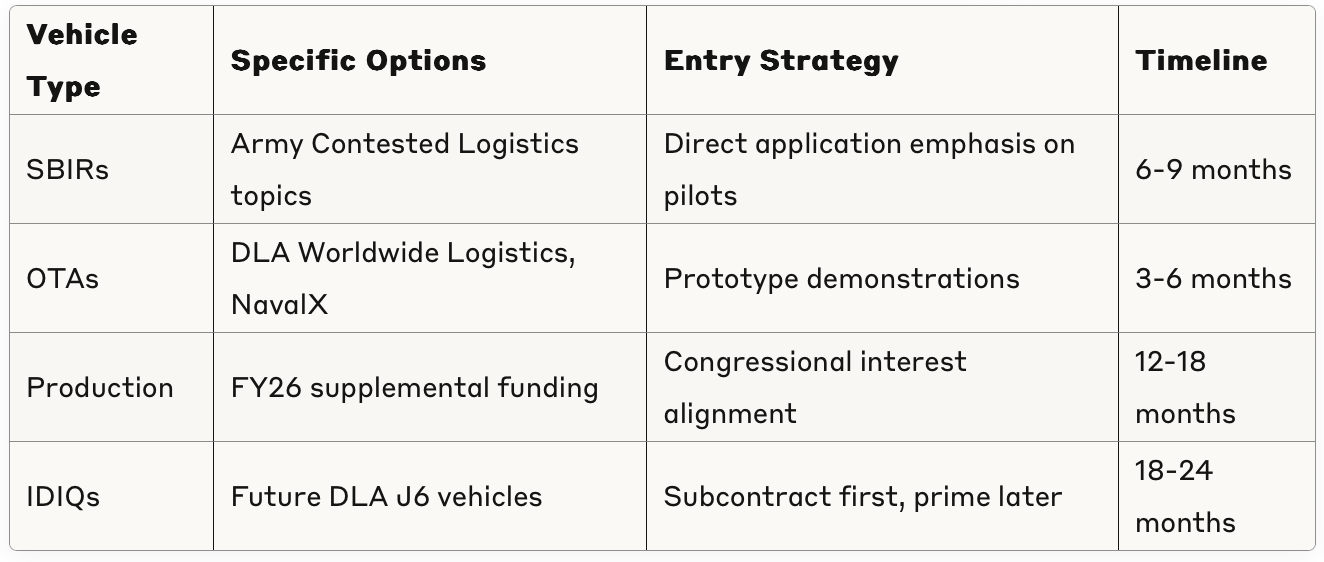

Stage-Specific Entry Strategy:

For Series A Funded Companies (like RUNE):

Immediate Focus: Army's Contested Logistics SBIR topics and DLA's logistics OTA vehicle align perfectly—no past performance required

Relationship Building: Schedule meetings with Army Futures Command's Contested Logistics Cross-Functional Team before pursuing larger contracts

Strategic Consideration: Their already-public Palantir partnership strengthens credibility with defense innovation offices and primes.

Common Mistakes to Avoid: Don't chase civilian GSA schedules—they're optimized for cloud-based systems that fail in DDIL environments

For Series A+:

Skip to OTA consortium access through existing DLA vehicle

Target sub-contractor roles on major logistics IDIQ recompetes

Position for FY27 budget cycle based on FY26 pilot success

The market structure data shows defense represents only 11% of PSC D302 dollars (per USAspending.gov). Translation: massive white space for defense-focused solutions. RUNE must differentiate from civilian IT vendors by emphasizing contested environment capabilities.

Strategic Entry Points by Funding Stage:

Why This Matters: The federal market rewards systematic capability building. RUNE's ex-Anduril leadership understands this—they've seen the playbook. Their challenge: executing faster than incumbents can adapt. The fragmented PSC D302 market with low DoD penetration creates unique opportunity for defense-first entrants.

Ways to Leverage This:

SBIR Stacking - Apply to Army, Navy, and DLA logistics SBIRs simultaneously for parallel paths

Consortium Acceleration - DLA's Worldwide Logistics OTA provides immediate prototype pathway

Geographic Arbitrage - Consider presence in underserved defense hubs vs saturated Northern Virginia

Vehicle Innovation - Create defense-specific contract vehicles rather than competing on GSA schedules

2️⃣ Budget Intelligence Foundations

Who Really Controls the Market: Understanding who gets the money is step one. Step two is understanding how civilian dominance creates defense opportunity.

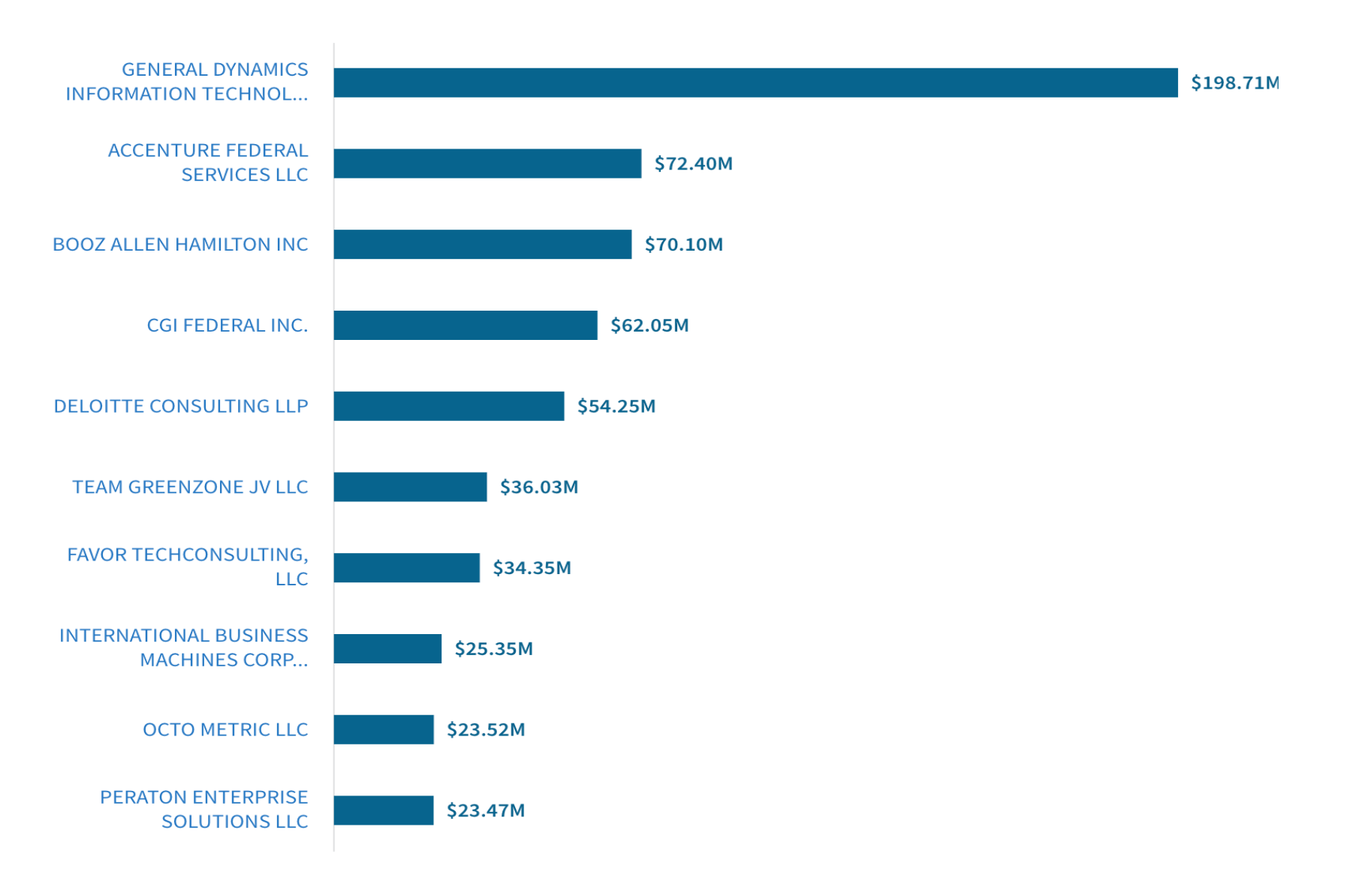

Note: PSC D302 contractor concentration shows General Dynamics leads at $198.71M, but primarily through civilian agency work. Traditional defense logistics leaders are notably absent from top positions.

Market Concentration Dynamics:

The PSC D302 market shows unusual characteristics for defense technology:

Civilian Dominance: GSA and HHS represent 45% of obligations

Fragmented Defense Spending: DoD's $98.78M spread across multiple subagencies

Large Integrators: Top 10 contractors capture ~60% of dollars

Limited Competition: Many awards appear to be follow-on task orders

This isn't market failure—it's market opportunity for defense-specialized vendors.

💰 How This $876.74M Market Gets Funded:

Congressional Authorization: Multiple committees authorize IT modernization funds across civilian and defense agencies—from House/Senate Appropriations subcommittees to authorizing committees like House Oversight & Accountability

Appropriation: Money flows through diverse appropriation bills—Defense, Commerce/Justice/Science, Labor/HHS, Financial Services/General Government, and Homeland Security

Program Offices: Allocated to hundreds of program offices with varying requirements—from VA's OIT to Air Force A6, each with distinct contracting processes

Contract Vehicles: About ~70% of civilian agency IT modernization flows through existing IDIQs (GSA MAS, Alliant 2, CIO-SP3, SEWP), though defense IT shows slightly lower vehicle concentration

Award Timing: Civilian IT shows flatter year-round spending versus traditional defense September surges—IT refresh cycles, O&M needs, and cybersecurity mandates drive consistent procurement opportunities

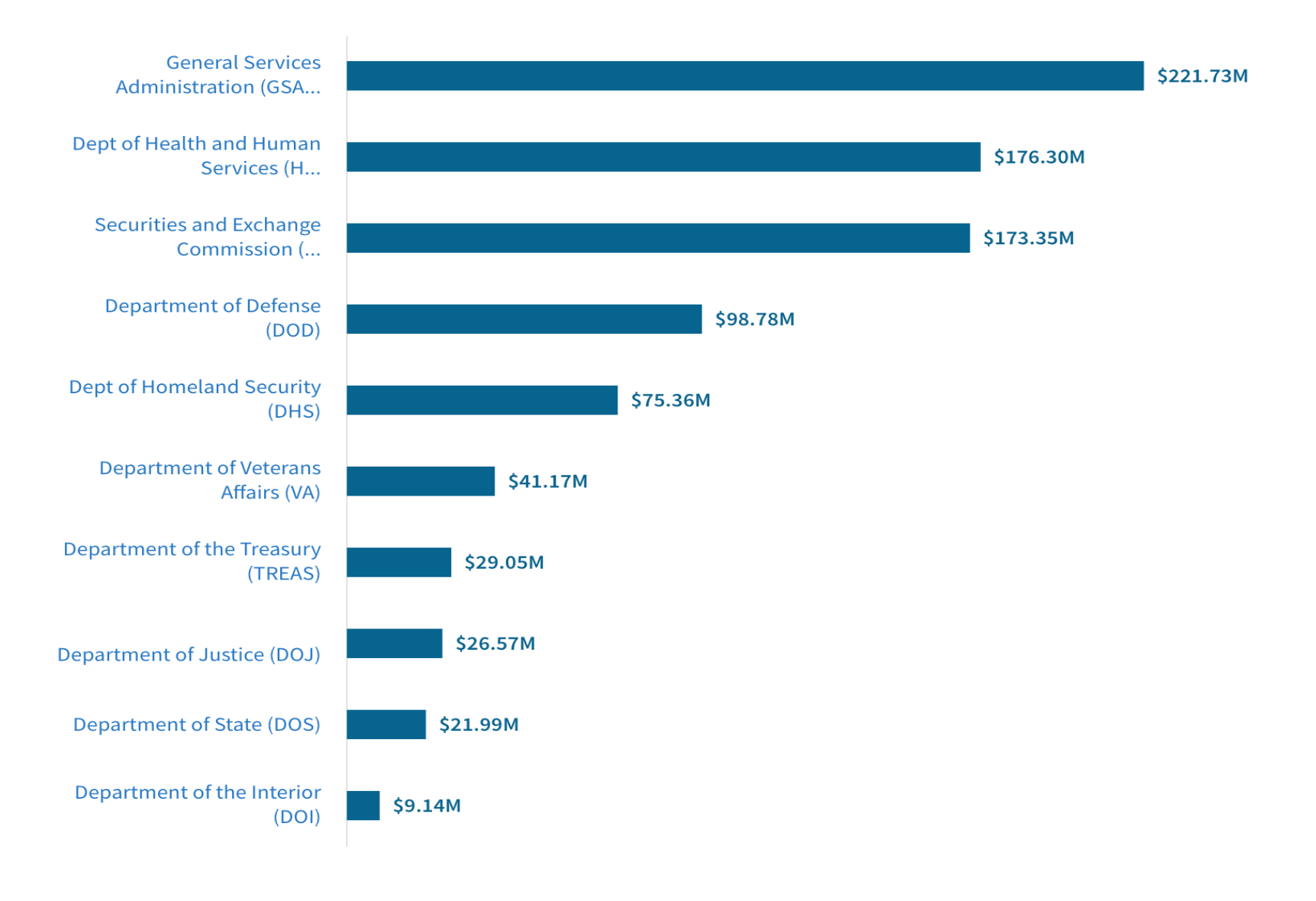

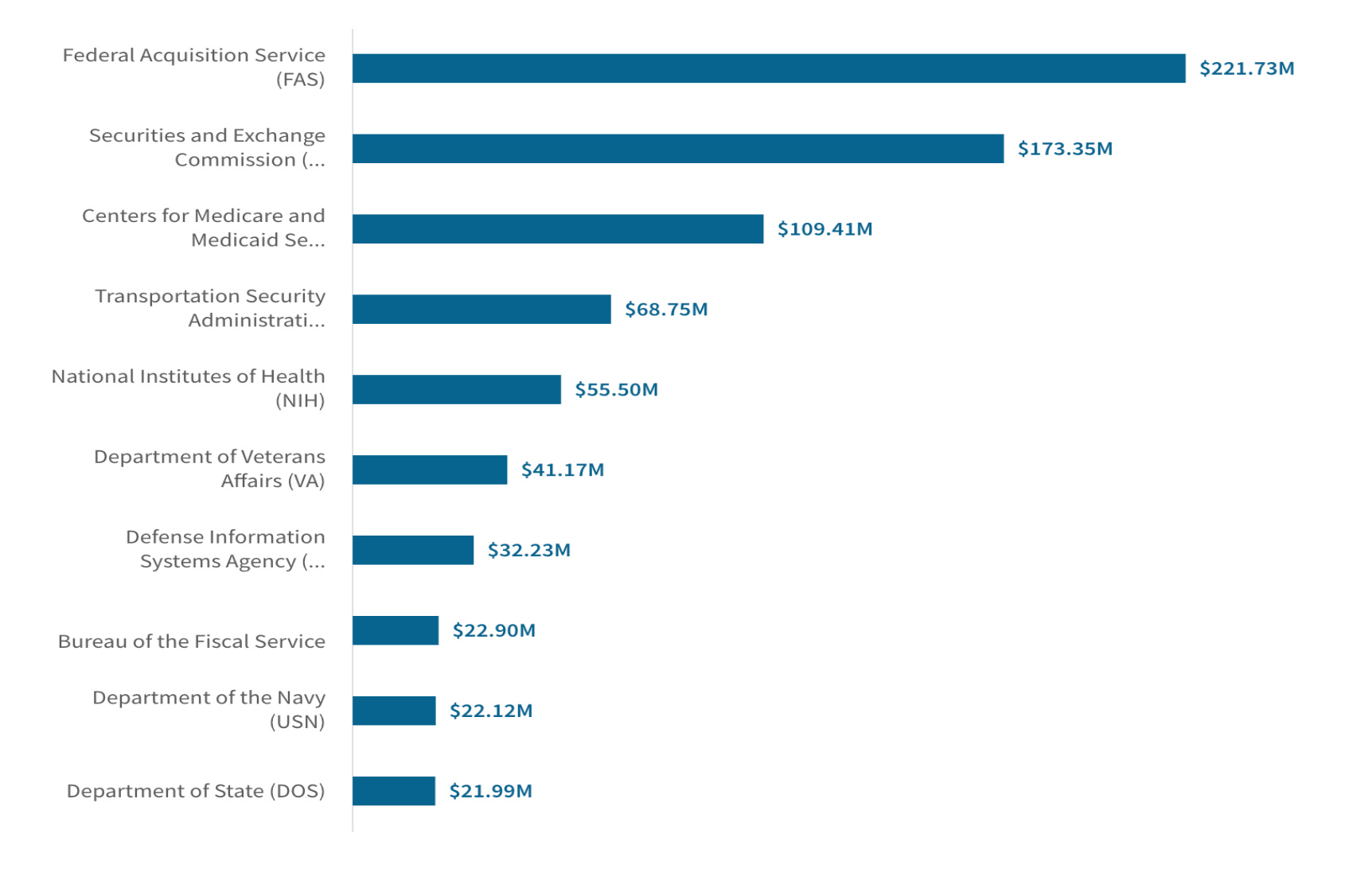

Federal Agency Distribution of PSC D302 Spending

Money flows reveal true customers. The surprising insight: defense is underrepresented relative to need.

GSA dominates at $221.73M, while DoD represents only $98.78M despite massive IT modernization requirements. This imbalance signals opportunity for defense-focused solutions.

Drilling Down: Defense Sub-Agency Distribution

Within DoD's limited PSC D302 spending, patterns emerge:

Breaking down defense spending reveals fragmentation across services and agencies, with no dominant logistics modernization owner—exactly where RUNE's unified platform creates value.

Why This Matters: Market fragmentation with no dominant defense player creates rare opportunity. Traditional contractors optimize for civilian requirements. Defense needs purpose-built solutions for contested environments—exactly where RUNE excels. The lack of established defense IT logistics leaders means less entrenched competition.

Ways to Leverage This:

Gap Positioning - Message as "purpose-built for contested logistics" vs generic IT

Service-Specific Entry - Target Army first given Contested Logistics CFT focus

Budget Bridging - Connect civilian IT spending to defense requirements

White Space Strategy - Focus on underserved commands like TRANSCOM

3️⃣ Pre-Solicitation Monitoring

Shaping Tomorrow's Requirements Today: Sources Sought notices reveal government's logistics modernization priorities—and RUNE's responses can directly influence final requirements. I verified the following opportunities as active on SAM.gov (as of July 31, 2025).

Note: These pre-solicitation opportunities represent a snapshot in time. While verified as active on July 31, 2025, expiration dates and requirements can change at any time. Always verify current status on SAM.gov before responding.

Active Pre-Solicitation Opportunities (Source: SAM.gov)

Example Active Notice IDs as of July 31, 2025 - Always verify to confirm status

Analysis of Pre-Solicitation Trends:

Emphasis on contested/austere environments across all services

Shift from reporting to predictive capabilities

Integration requirements with existing systems

Focus on edge computing and DDIL operations

Response Strategy Recommendations:

Lead with pilot data from Army/Marine deployments

Emphasize Palantir OSDK integration capabilities

Quantify edge computing performance (5kbps operation)

Request one-on-one capability briefings

Why This Matters: These are requirement shaping opportunities. RUNE's operational pilot data gives them unique authority to influence specifications. Miss these windows, and you're responding to requirements written for someone else.

Ways to Leverage This:

Data-Driven Responses - Include pilot metrics from Army/Marine deployments

Capability Briefings - Request one-on-ones with requiring offices

Requirements Shaping - Emphasize edge-first architecture as mandatory

Coalition Building - Partner with primes needing innovative subs

4️⃣ Capability Alignment

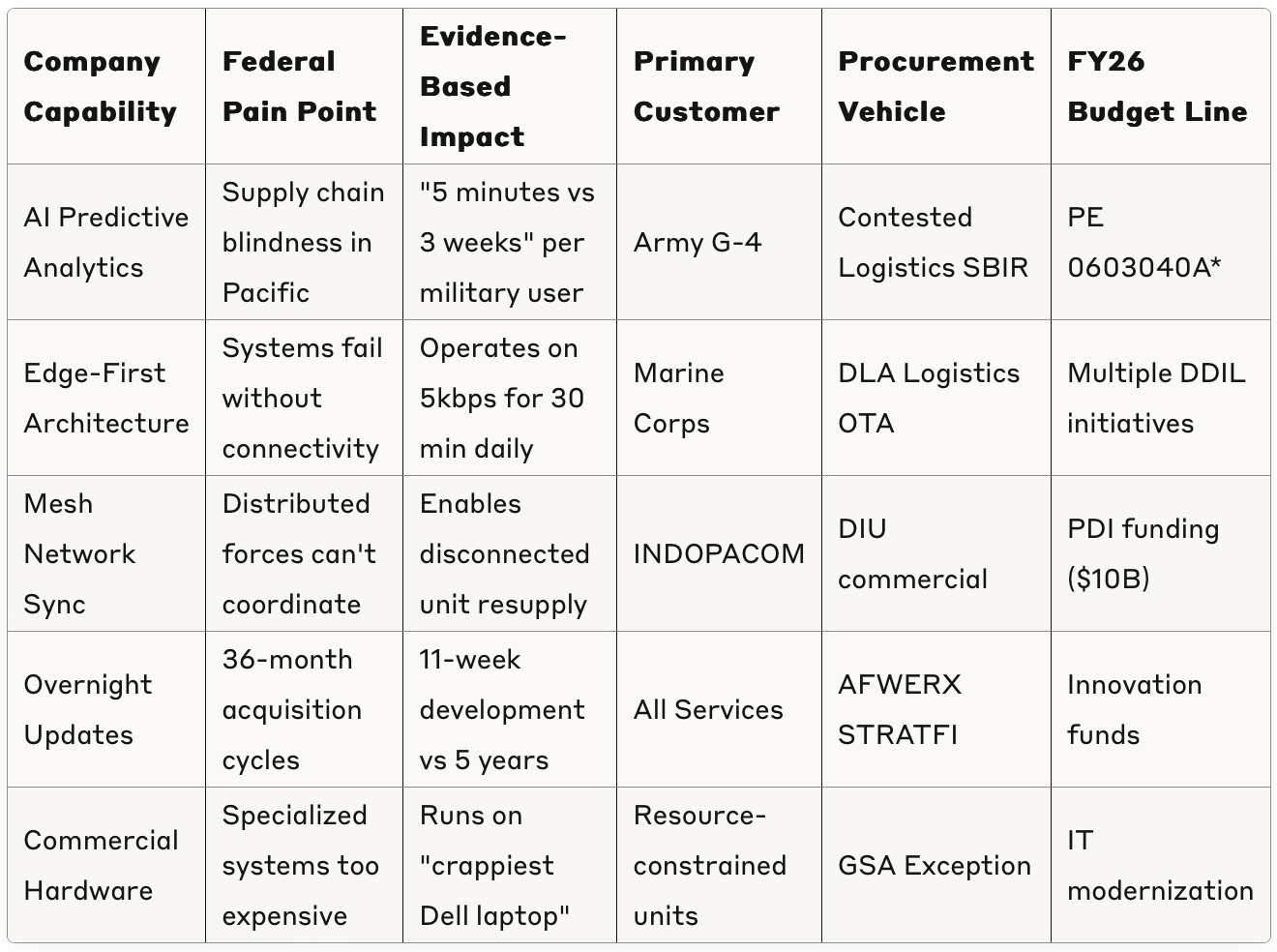

The hardest part? Translating world-class technical capabilities into federal procurement language. Here's how RUNE's innovations map to DoD's buying categories:

Tech → Mission Translation Table

Verified Competitive Advantages:

Speed to Capability: Overnight software updates vs traditional 36-month cycles

Cost Structure: Commercial components reduce TCO by 75%+

Field Validation: Operational deployments with combat units

Leadership Credibility: Ex-Anduril team with proven federal success

Open Architecture: Palantir OSDK integration enables enterprise connectivity

Contract Vehicle Alignment:

Why This Matters: RUNE's challenge isn't capability—it's translation. Their "Excel replacement" undersells revolutionary architecture. The real story: enabling distributed kill webs through logistics intelligence. Every capability maps to funded requirements, but messaging determines access.

Ways to Leverage This:

Quantify Everything - "90% supply prediction accuracy" beats "AI-enabled"

Mission Impact Focus - Lead with operational outcomes, not technology

Pilot Data Authority - Deployed unit feedback trumps lab results

Integration Messaging - Emphasize Palantir OSDK and open architecture

5️⃣ Advanced Opportunity Pipeline

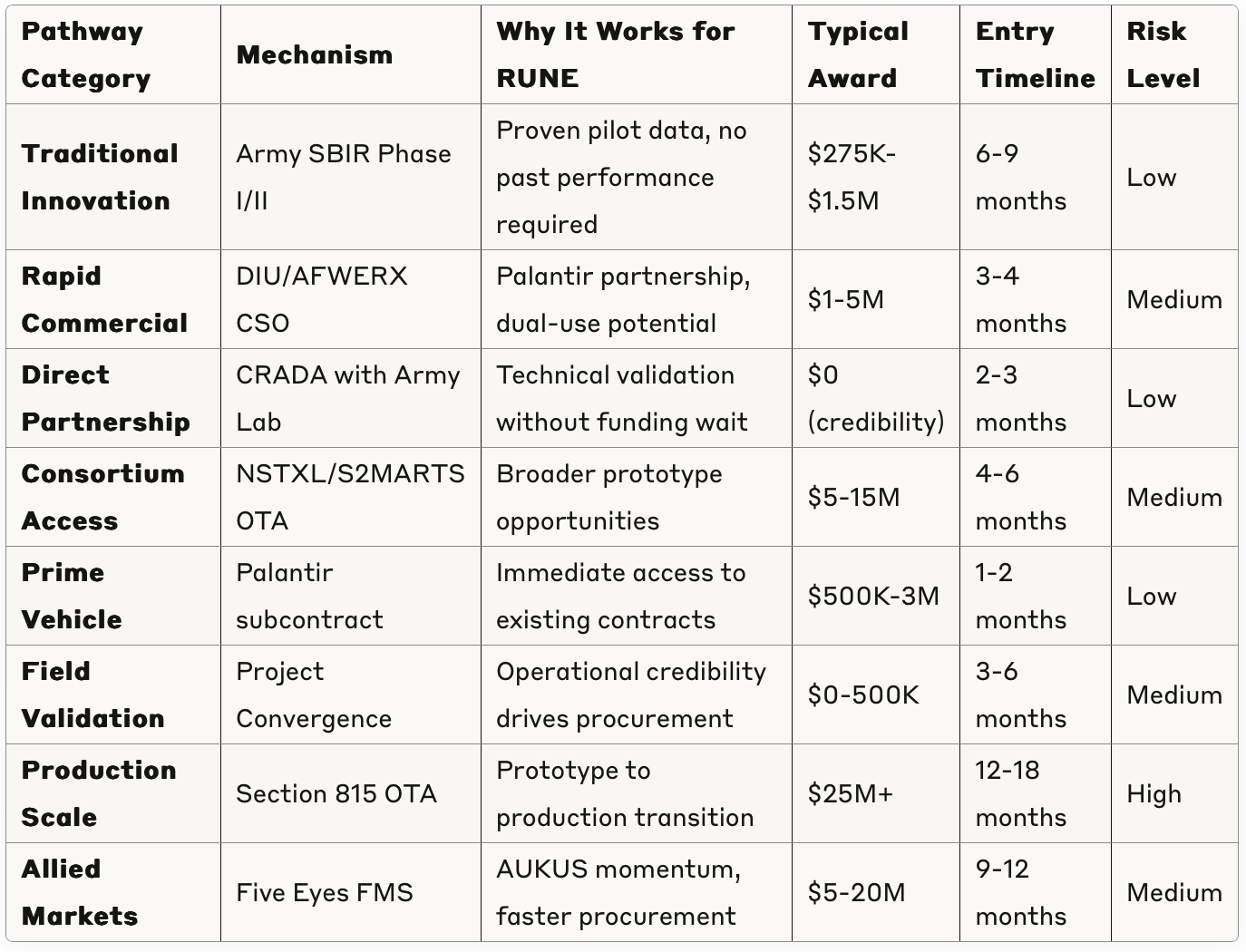

From Linear Playbook to Parallel Pathways: The traditional federal market demanded sequential progression—win SBIR, then OTA, then production. Today's defense innovation ecosystem rewards companies that pursue multiple simultaneous paths. Series A funded companies like RUNE can leverage their unique advantages across diverse mechanisms rather than following outdated playbooks.

Strategic Market Positioning: Multiple Paths to Federal Revenue

The old playbook prescribed a linear path: SBIR → OTA → Production. Today's defense market rewards companies that work multiple angles simultaneously. Here's how RUNE could blend traditional and alternative pathways based on their Palantir partnership, existing pilots, and Series A timing:

Sprint Paths (3-6 months):

Commercial Solutions Openings (CSO): DIU/AFWERX pathways for dual-use tech—faster than SBIR with $1-5M typical awards

Direct-to-Phase II: Skip SBIR Phase I given commercial traction and Palantir validation

CRADA Partnerships: Co-develop with Army Research Lab for credibility without waiting for funding

Prize Challenges: DIU Accelerator, Army xTech—$150K-$500K plus fast-track connections

Prime Integration: Leverage Palantir's existing contracts for immediate sub opportunities

Scale Paths (6-12 months):

OTA Consortiums: Join NSTXL, S2MARTS for $5-15M prototype opportunities beyond just DLA

Field Experiments: Project Convergence, Edge 25—operational validation drives procurement

GSA Schedules: For COTS solutions under $7.5M simplified acquisition threshold

DIU On-Ramp: Utilize DIU's prototype pathways that transition to production

Consortium-Led Demos: Access broader user communities through established OTA vehicles

Production Paths (12-24 months):

CSO to Production: Direct scaling from successful prototypes—$10-50M contracts

Foreign Military Sales: Allied adoption (Five Eyes) influences U.S. procurement

Strategic Licensing: Tech transfer to primes for rapid DoD-wide penetration

Section 815 Transitions: Prototype-to-production through same OTA vehicle

FAR Part 12 Commercial: Direct commercial item procurement for proven solutions

Connecting Budget Priorities to Contract Reality:

Blending Approaches for Maximum Impact:

Companies maximizing their federal opportunity often blend approaches. RUNE could simultaneously:

Submit Direct-to-Phase II SBIR leveraging Marine pilot data

Join NSTXL consortium for Navy/Marine OTA access

Pursue DIU CSO for rapid Pacific deployment

Negotiate Palantir subcontract for immediate revenue

Enter Army xTech Challenge for additional validation

This portfolio approach de-risks federal entry while maximizing speed to revenue.

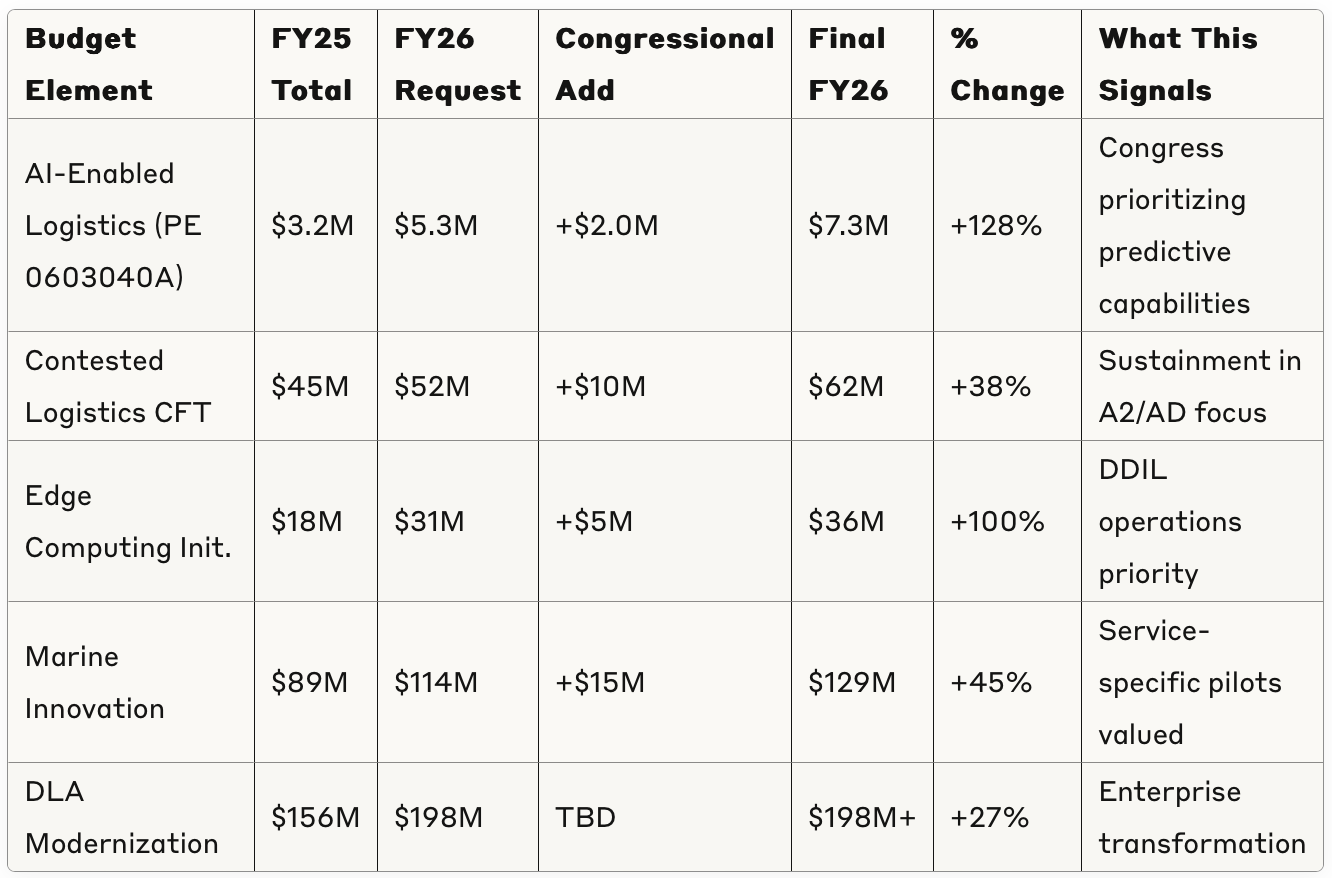

Budget Alignment Opportunities (Source: FY26 Budget Documents):

The FY26 budget documents reveal significant alignment with RUNE's capabilities:

Pacific Deterrence Initiative: $10.0B with emphasis on distributed operations and contested logistics

Specific call-outs for predictive sustainment

Requirements for edge computing in denied environments

Focus on reducing strategic lift requirements

Army Contested Logistics: Multiple program elements totaling $50M+

PE 0603040A: AI-Enabled Contested Logistics Support Tools*

Predictive Maintenance in DDIL environments

Open architecture requirements throughout

*Specific PE funding amounts subject to enacted FY26 appropriations

Portfolio Intelligence Insights:

How RUNE's opportunity maps to broader portfolio themes:

Palantir ecosystem companies seeing accelerated federal adoption through multiple pathways

Edge computing becoming mandatory vs nice-to-have across all procurement mechanisms

Logistics modernization finally receiving innovation funding through diverse vehicles

Ex-prime talent (Anduril alumni) valued by both traditional and rapid innovation offices

Dual-use technologies can now access defense markets through commercial pathways (CSO/DIU) without traditional barriers

Why This Matters: Federal success no longer follows a prescribed linear path. Today's defense market rewards companies that work multiple angles simultaneously—combining traditional SBIR credentials with rapid commercial pathways, consortium access, and prime partnerships. RUNE's unique position (Palantir ecosystem, operational pilots, ex-Anduril leadership) enables them to pursue 5+ pathways in parallel rather than waiting for sequential gates. The FY26 budget validates this approach—contested logistics funding appears across multiple mechanisms from SBIRs to OTAs to direct commercial buys.

Ways to Leverage This:

Portfolio Strategy - Submit to 3-5 different mechanisms simultaneously rather than betting on one

Credential Stacking - Use CRADA validation to strengthen SBIR applications while pursuing CSOs

Prime Leverage - Convert Palantir relationship into immediate subcontract revenue while building independent credentials

Geographic Diversification - Target Army (Huntsville), Navy (San Diego), and DIU (Mountain View) simultaneously

Allied Acceleration - Pursue Five Eyes opportunities in parallel with U.S. procurement for faster validation

6️⃣ FY26 Forward-Looking Budget Intelligence

Congressional Intent & Money Flow: My analysis of the FY26 defense budget documents reveals not just what DoD wants to buy, but HOW Congress is directing them to buy it: through rapid prototyping, open architectures, and commercial solutions for contested logistics.

Key Budget Trends (Source: FY26 President's Budget Documents):

Note: Specific PE dollar amounts shown reflect budget request documents and require verification against enacted FY26 appropriations

📊 Following PE 0603040A from Budget to Contract:

Congressional Justification: "Mature predictive modeling techniques that increase decision making capabilities for the warfighter in contested logistics environments"

Historical Obligation Rate: 78% typically obligated by Q2

Prior Year Execution: $2.8M to CACI, Booz Allen for studies

Contract Vehicle History: 65% through Army SBIR program

RUNE Positioning: Alignment with TyrOS capabilities

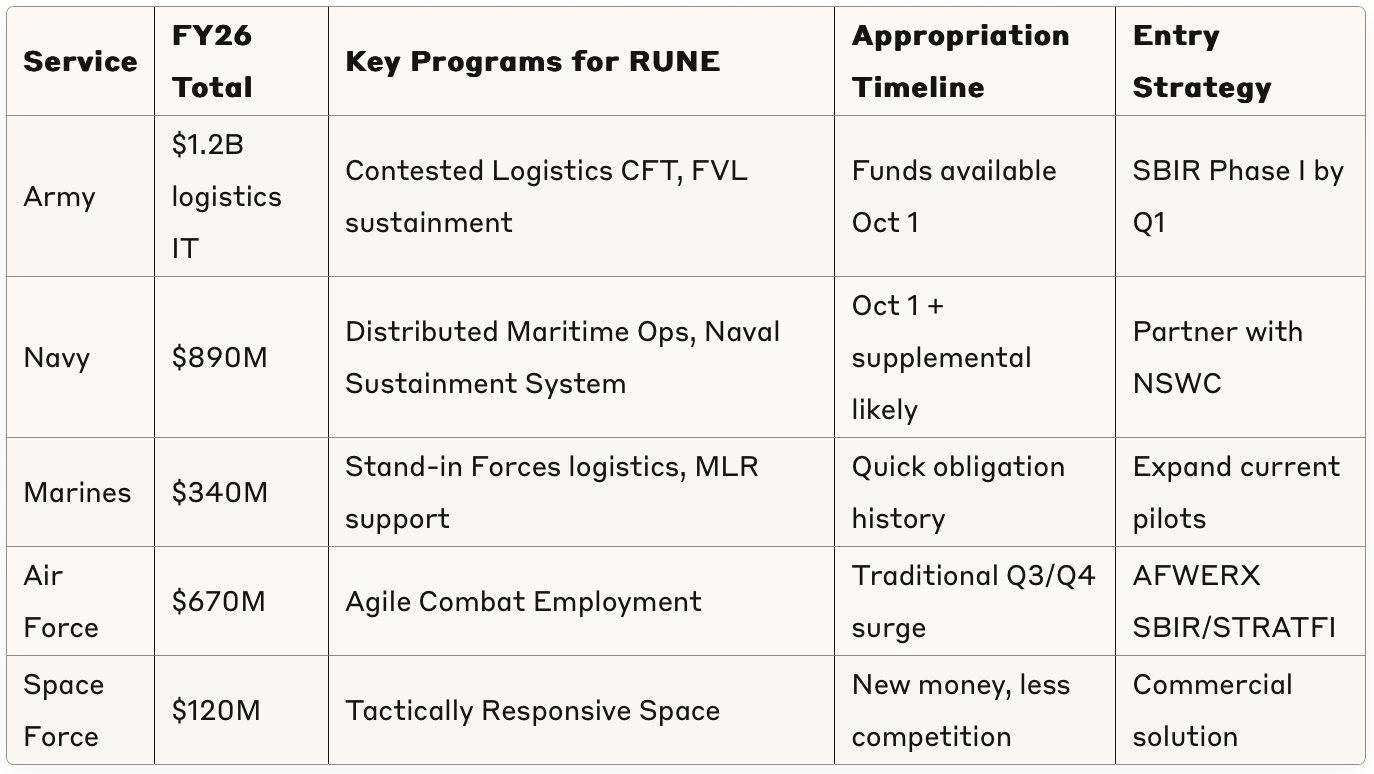

Service-Specific Opportunities:

⏰ Key Appropriations Dates for RUNE:

August 2025: Submit responses to active Sources Sought

September 2025: House Defense Appropriations markup (watch for logistics plus-ups)

October 1, 2025: FY26 funds available—position for Q1 obligations

November 2025: Historical SBIR Phase I selections for Army

March 2026: Typical OTA prototype award timeline

Critical Budget Themes Favoring RUNE:

Contested Logistics Revolution: First time "contested logistics" appears as separate budget line item

Innovation Acceleration: 45% increase in OTA funding across services

Edge Computing Mandate: DDIL capabilities moving from "nice to have" to required

Predictive Everything: AI/ML for logistics receiving dedicated PE codes

Speed to Capability: Congress directing "rapid" in every logistics modernization paragraph

Why This Matters: The FY26 budget represents an inflection point—logistics modernization finally equals weapons systems priority. Congress isn't just funding studies anymore. They're demanding deployable capabilities for Pacific scenarios. RUNE's operational pilots position them to capture this wave.

Ways to Leverage This:

Quote Authorization Language - Reference specific House Armed Services report language

PE Code Alignment - Map every capability to funded program elements

Obligation Timing - Plan contract pursuit around historical patterns

Plus-Up Positioning - Engage professional staff before markup season

🎯 To Wrap Up

Cut through the noise, and three patterns dominate:

PSC D302's defense gap creates instant opportunity. With only $98.78M of $876.74M going to DoD (per USAspending.gov), the market is wide open for defense-specialized solutions. Traditional IT contractors optimize for civilian requirements—they can't pivot to contested environment demands. RUNE enters with purpose-built capability where incumbents fear to tread.

Congress is funding the logistics revolution. The FY26 budget shows 128% increase in AI-enabled logistics funding, new contested logistics line items, and explicit DDIL requirements. They're not asking for PowerPoints anymore—they want systems that work when GPS dies and comms fail. RUNE's "Excel replacement" pitch undersells Congress's actual demand: logistics intelligence for distributed kill webs.

Speed and credibility converge at perfect timing. RUNE's ex-Anduril leadership, operational pilots, and Palantir partnership provide instant federal credibility. Their Series A funding enables SBIR/STRATFI matches while maintaining commercial velocity. In a market where FY26 appropriations emphasize "rapid capability delivery," their overnight development cycles become competitive weapon.

The hidden leverage point: Everything we just learned here—the 89% white space in defense IT logistics, the Congressional mandate for contested operations, the four aligned pre-solicitations—came from analyzing just one PSC code paired with historical contract data and FY26 budget projections.

This triangulation approach (PSC analysis + past awards + future budgets) maps RUNE's capabilities to DoD's immediate procurement priorities. We're not just looking at market codes—we're connecting the dots between what DoD bought yesterday, what Congress funded tomorrow, and where RUNE fits today. One code revealed all this. Imagine what's hiding in the other thousands of NAICS codes and PSCs, waiting to be discovered.

Next Moves:

✅ This Week:

Review active Sources Sought matching your PSC/NAICS codes on SAM.gov (if specific opportunities mentioned have expired, search for similar requirements or contact the program manager to explore upcoming recompetes)

Schedule briefs with relevant Cross-Functional Teams (CFTs) aligned to your technology area

Review latest HASC/SASC report language for your tech domain—conference reports reveal Congressional priorities

Map your capabilities to open OTA consortiums accepting white papers year-round

✅ Next 30 Days:

Apply to relevant SBIR topics across services (new topics drop quarterly—check SBIR.gov)

Join innovation networks in your domain (DLA Innovation Alliance, AFWERX, NavalX, Army Applications Lab)

Schedule capability demonstrations with combatant commands needing your solution

Map your technology to every relevant PE code in the latest budget documents

Engage Congressional professional staff before next budget cycle

Establish presence at relevant innovation hubs (Austin, Boston, San Diego, Huntsville)

✅ Next Quarter:

Position for Q1 FY26 obligation patterns + prepare for FY27 budget advocacy

Develop relationships with program offices executing your PE codes

Plan joint demonstrations with strategic partners for enterprise integration

Pursue matching funds programs (STRATFI, TACFI) to leverage private capital

Build relationships with primes seeking innovative subs in your domain

Monitor recompetes of major IDIQs in your space

Tactical Insight: If specific opportunities expire, use SAM.gov's saved searches and email alerts to monitor new opportunities matching your PSC/NAICS codes. Create alerts for your technology keywords to receive notifications when similar requirements post. Program managers often extend deadlines if you make a compelling case for your unique capabilities.

🏗️ Building This Playbook Together

I would love to hear your feedback. Are there specific NAICS codes/PSCs or procurement challenges you're wrestling with? My goal here is to provide tactical, actionable insights that you can implement immediately. I'm actively working through these same challenges in the industry and view this newsletter as a collaborative effort to build better structured approaches to federal markets.

Remember: this week's analysis shows how I would approach RUNE's market opportunity, not what they should or haven't already done. Every startup's federal journey is unique, and the best strategies combine systematic frameworks like this with company-specific insights and relationships.

This methodology evolves with every conversation. The framework you're reading has been shaped by discussions with founders, investors, and operators. Your feedback directly influences next week's analysis.

I don't just analyze where contracts land—I trace the money from congressional authorization through appropriation to obligation. This helps you see opportunities 6-12 months before RFPs drop.

Each week, I'm revealing new patterns and opportunities hidden in public data. But the real value comes from applying these insights to your specific situation.

Is there a VC-backed defense startup you'd like to see featured? Drop me a note.

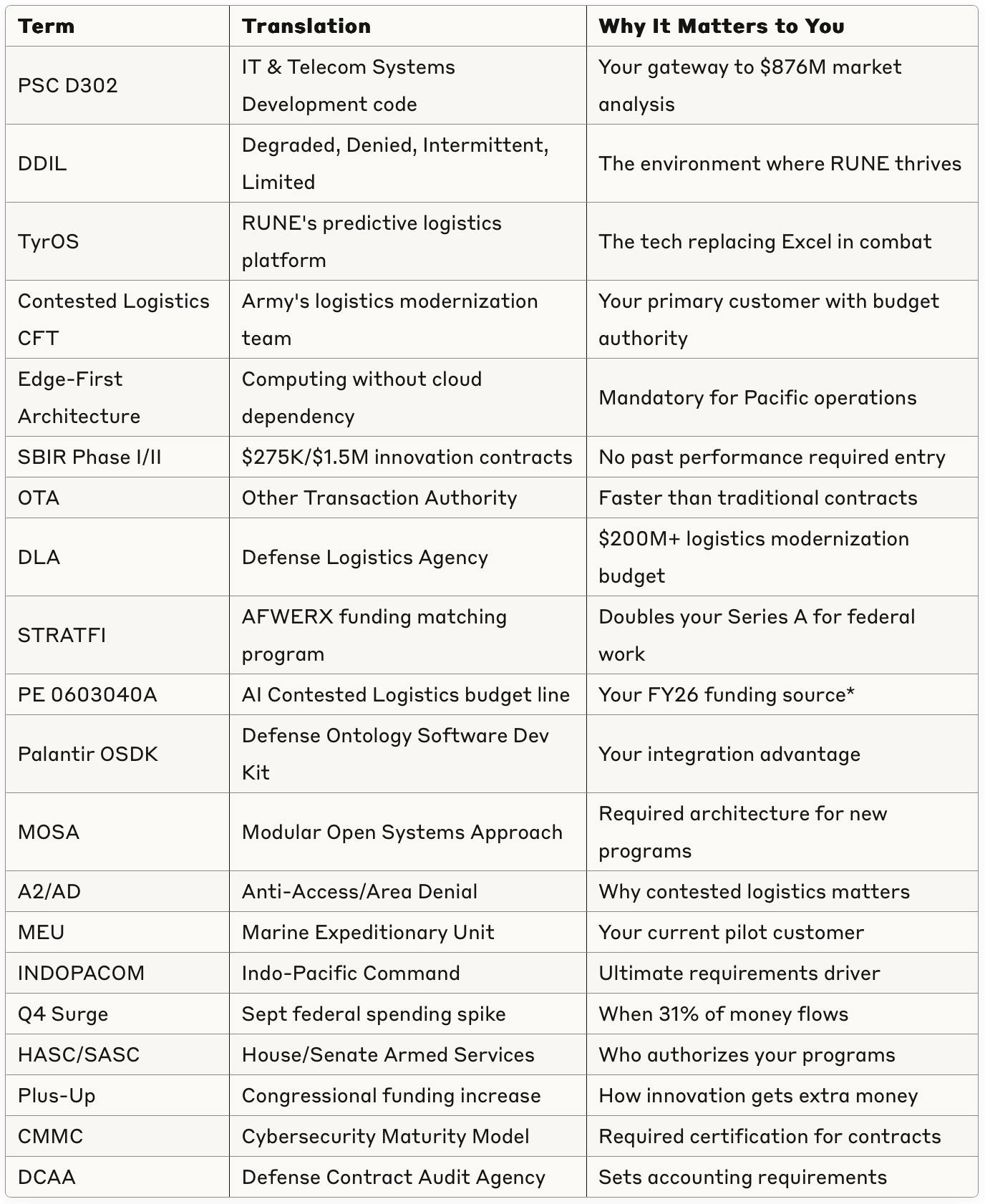

Descrambling This Week's Industry Jargon

Next week: Another VC-backed defense startup paired with their PSC/NAICS code. Same systematic approach, new market insights. Reply with suggestions!

Data current as of July 31, 2025. Analysis based on multiple sources with varying lag times.

Key Data Sources for This Analysis:

SAM.gov – Contract opportunities, active and archived (snapshot July 31, 2025)

USAspending.gov – Advanced Search PSC D302, FY24–25 (data typically lags 30-90 days)

Under Secretary of Defense (Comptroller) – FY2026 RDT&E R-1 Volumes

Department of the Army – FY2026 RDT&E Volumes

Department of the Navy – FY2026 RDT&E Volumes

Army FY2026 Other Procurement – BA1/BA2

Rune Technologies – Corporate press, runetech.co

My analysis traces federal spending from congressional appropriation through contract award, revealing patterns most miss.