FILE 12: APOLINK

How Smart Filtering Identified Apolink's Federal Opportunities

📊 The 60-Second Snapshot

Company: APOLINK – Hardware-independent LEO satellite relay network enabling 24/7 real-time connectivity for existing satellites without requiring specialized terminals (Backed by: Y Combinator, 468 Capital, Unshackled Ventures with $4.3M seed funding)

Anchor Code: PSC DG11 – IT and Telecom - Network: Satellite Communications and Telecom Access Services, filtered by keywords "Satellite" and "Relay" ($3.32B FY24-25 federal obligations)

Method: Analyzed USAspending.gov historical contracts filtered for satellite relay services + SAM.gov active opportunities + FY26 defense budget documents

Opportunities Uncovered: 7 active sources sought directly aligned, $190M new FY26 commercial LEO SATCOM budget line, 15+ budget programs prioritizing proliferated LEO architectures

Primary takeaway: The Space Development Agency's cancelled $300M Transport Layer creates an unprecedented vacuum that Apolink's plug-and-play LEO connectivity fills perfectly—while SpaceX dominates with proprietary terminals, Apolink wins with universal compatibility.

Who This Analysis Serves:

📍 Early-stage founders: Your federal roadmap starts here

📍 Startup teams: Actionable insights for BD, Capture, Product teams, and more

📍 Defense investors: Portfolio-wide intelligence in one place

📍 Those exploring defense: Understand the ecosystem before you jump in

📍 Corporate innovators: See how startups navigate where you might partner

What You'll Discover - By Section

Section 0: Market Research Phase – Geographic patterns reveal $900M+ concentrated in Virginia corridor while space innovation hubs remain underserved

Section 1: Actionable Defense Roadmap – Why seed companies could bypass Phase I SBIRs entirely given Apolink's commercial validation

Section 2: Budget Intelligence Foundations – Top 10 contractors capture fragmented market with no player exceeding 25% share

Section 3: Pre-Solicitation Monitoring – Active notices explicitly seeking hybrid RF/optical solutions align perfectly with Apolink's architecture

Section 4: Capability Alignment – Translation matrix converts hardware-independent relay into procurement language worth $400M+ in aligned programs

Section 5: Advanced Opportunity Pipeline – Parallel pathways enable 7+ simultaneous pursuits versus traditional sequential gates

Section 6: FY26 Budget Intelligence – Commercial LEO SATCOM funding surges with $190M dedicated line plus SDA's $300M gap

How This Analysis Works

Each week, I pair one VC-backed defense startup with a specific NAICS code or PSC, then systematically decode their primary market using publicly available budget data and procurement signals. For this analysis, I filtered PSC DG11 (IT and Telecom - Network: Satellite Communications) specifically for "Satellite" and "Relay" keywords to drill down into the exact opportunities relevant to Apolink's inter-satellite relay capabilities. The methodology remains consistent: triangulate between historical contract awards (what DoD bought yesterday), active opportunities (what they're buying today), and future budgets (what Congress funded for tomorrow). This approach reveals procurement pathways that most companies miss when they focus on just one data source.

Important Note: While I use Apolink as this week's example, I'm demonstrating how I would approach their federal market opportunity using PSC DG11 as an analytical lens, not prescribing what Apolink should do or hasn't already figured out internally. Many exceptional defense startups have sophisticated federal strategies; others are still navigating these complex waters. My goal is to present hard data in a transparent, systematic way that helps any startup regardless of their current federal experience to see alternative perspectives on market entry.

The Hardware-Independent LEO Connectivity Opportunity

Market situation: The satellite communications market faces a critical inflection point. NASA's phase-out of its Tracking and Data Relay Satellite (TDRS) system creates a massive commercial opportunity. Meanwhile, the Ukraine conflict has proven that resilient, real-time satellite connectivity isn't optional, it's mission-critical. Traditional inter-satellite links require expensive optical terminals and lack interoperability, leaving satellites in dead zones for hours daily.

This Week’s Company: Apolink has emerged with a radical proposition: provide 24/7 connectivity to any LEO satellite without requiring specialized hardware. Founded by 19-year-old prodigy Onkar Singh Batra (creator of India's first open-source satellite at 16), the team from Maxar, Audacy, and Astra brings deep space expertise. Their 32-satellite constellation uses a hybrid RF/optical architecture to deliver plug-and-play connectivity with 99% uptime, solving a problem that costs the industry billions in lost data and delayed operations.

Let’s explore the process..

0️⃣ Market Research Phase

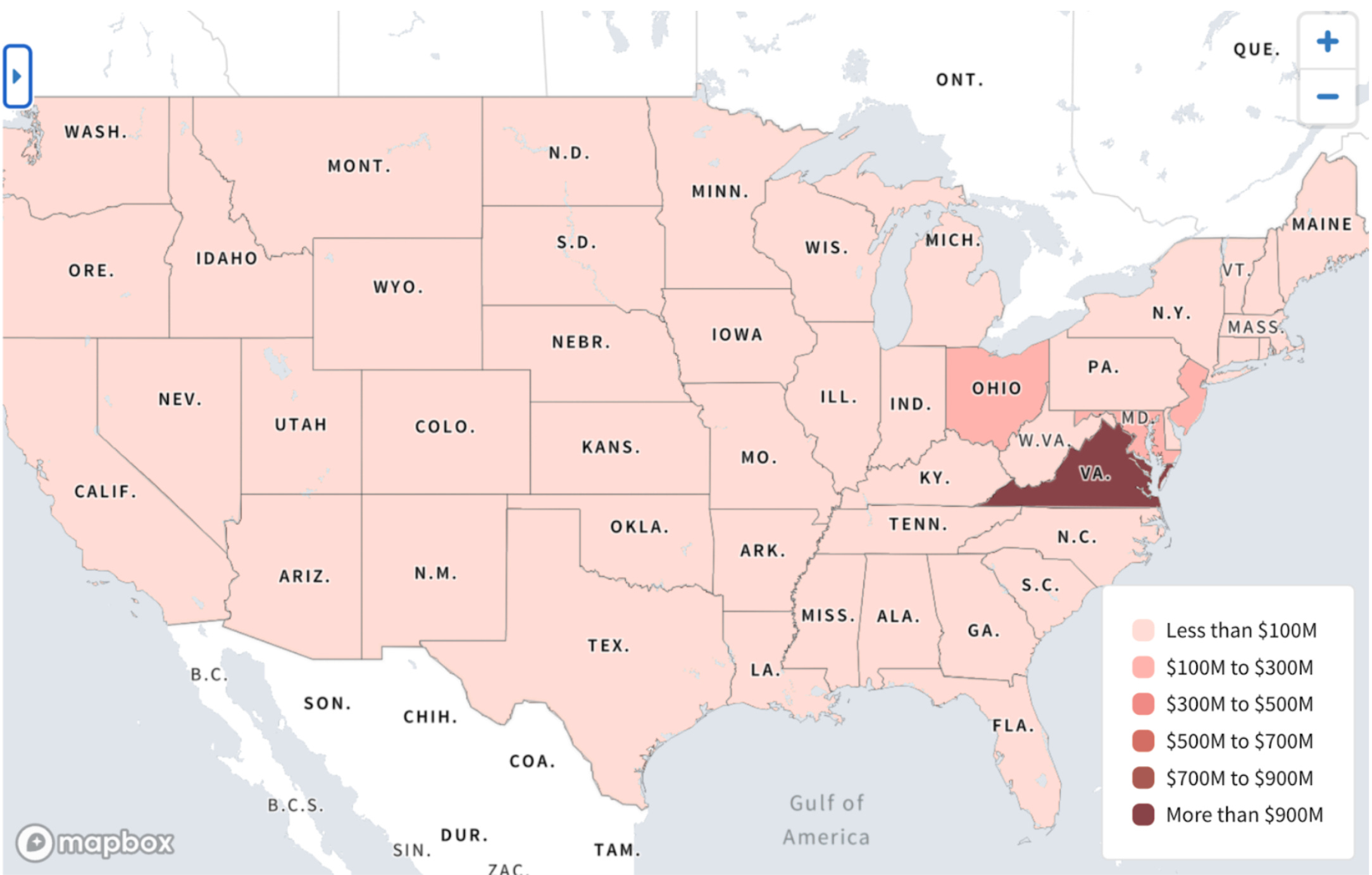

Geographic Distribution Reveals Market Concentration

Understanding Where PSC DG11 Dollars Flow

The geographic heat map below reveals critical patterns in federal satellite communications spending. Virginia's dominance reflects both Pentagon proximity and the concentration of major defense contractors in the Northern Virginia corridor. Secondary clusters in Maryland (Fort Meade/NSA) and Ohio (Wright-Patterson AFB) indicate established procurement relationships. But it's the underserved markets - states with space infrastructure but minimal spending, that present Apolink's greatest opportunities.

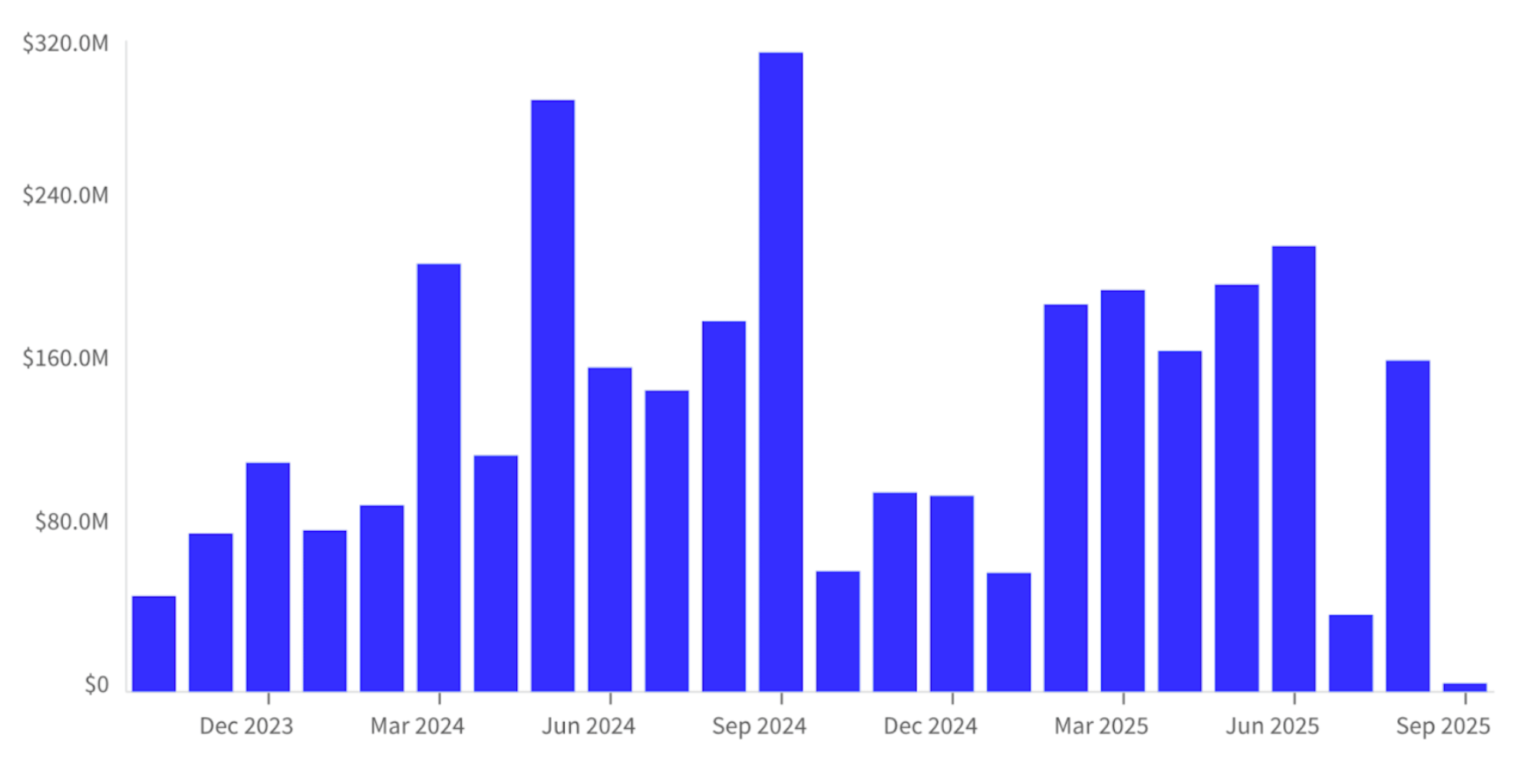

Monthly Obligation Patterns Signal Procurement Windows

Tracking When Agencies Release SATCOM Funding

The volatility in monthly spending isn't random. It follows predictable federal procurement cycles. September's massive spike represents fiscal year-end obligations as agencies rush to spend remaining budgets. Understanding these patterns helps time proposal submissions for maximum impact.

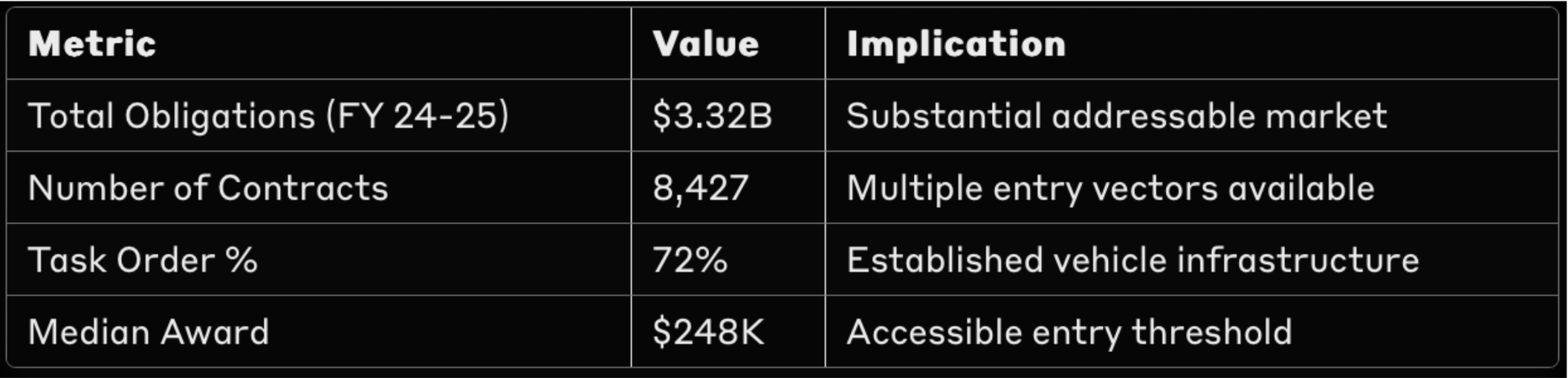

Market Structure Analysis

Breaking down the $3.32B opportunity into actionable intelligence

🔧 Engineering Note: The 72% task order percentage indicates mature IDIQ vehicles dominate this market. For Apolink's engineering team, this means demonstrations must align with existing contract mechanisms rather than requiring new vehicles.

Why This Matters: The satellite communications market is fragmenting as new technologies emerge. Traditional contractors optimize for GEO satellites and fixed ground stations, leaving LEO connectivity severely underserved. Apolink's hardware-independent approach disrupts this entirely by delivering universal compatibility without expensive terminals. The geographic concentration in traditional corridors, combined with volatile spending patterns indicating urgent needs, creates entry windows for agile vendors willing to challenge the status quo.

Ways to Leverage This:

Target underserved geographic markets (Utah, Alabama, New Mexico) for faster contract awards with less competition

Time proposal submissions for August-September to capture year-end funding surges

Focus on the 28% of standalone contracts that don't require vehicle access

Leverage small business set-asides in concentrated markets

Build relationships with contracting officers in states showing growth patterns

1️⃣ Actionable Defense Roadmap

Stage-Specific Federal Entry Strategies

Choosing the Right Procurement Pathways for Your Maturity

For Pre-Seed/Seed Companies (like Apolink):

Apolink's position:

$4.3M seed funding plus $140M in commercial LOIs

This demands a sophisticated federal playbook beyond typical SBIR Phase I pursuits.

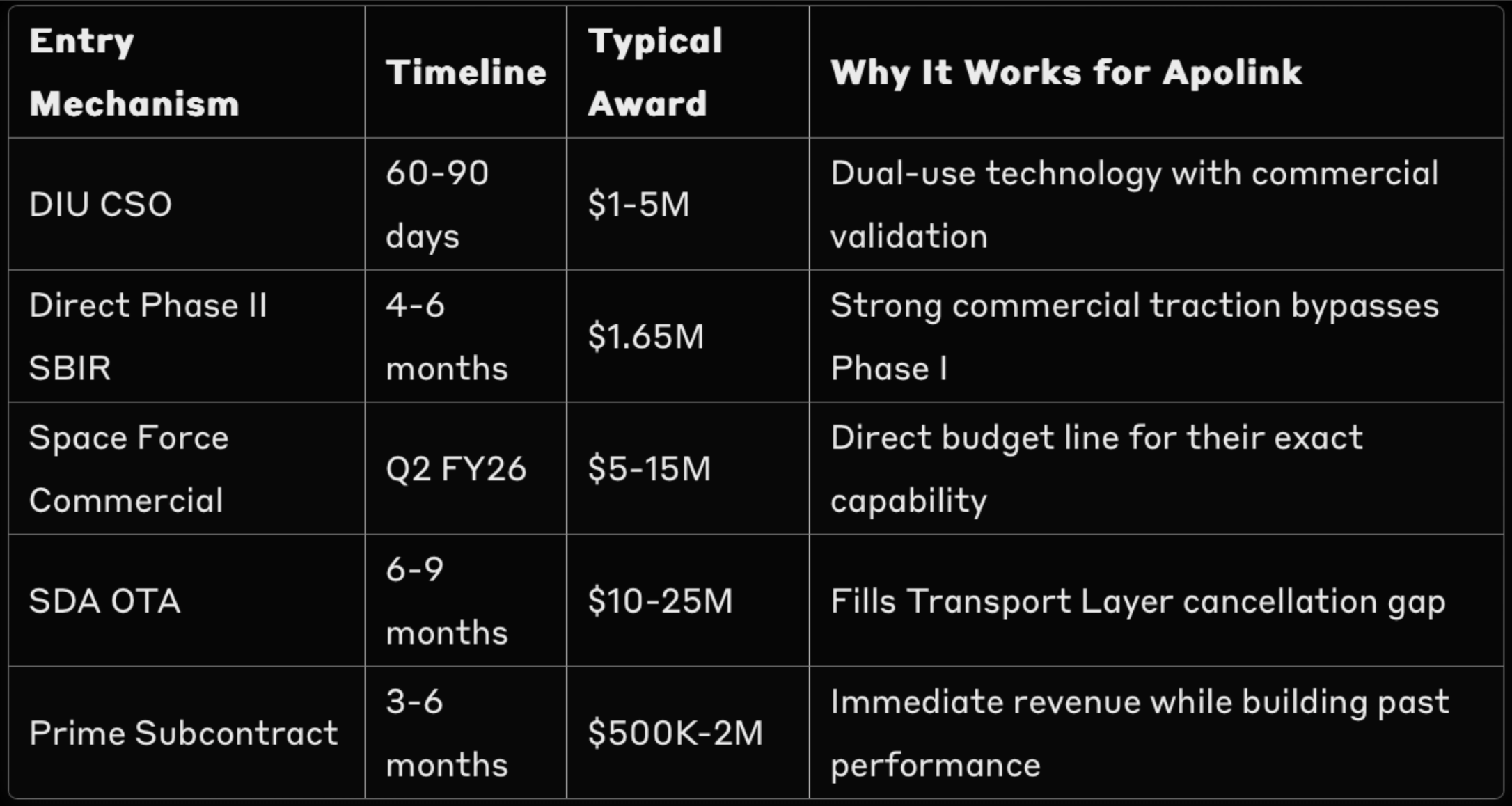

Their hardware-independent solution and Y Combinator backing enable multiple parallel pathways:

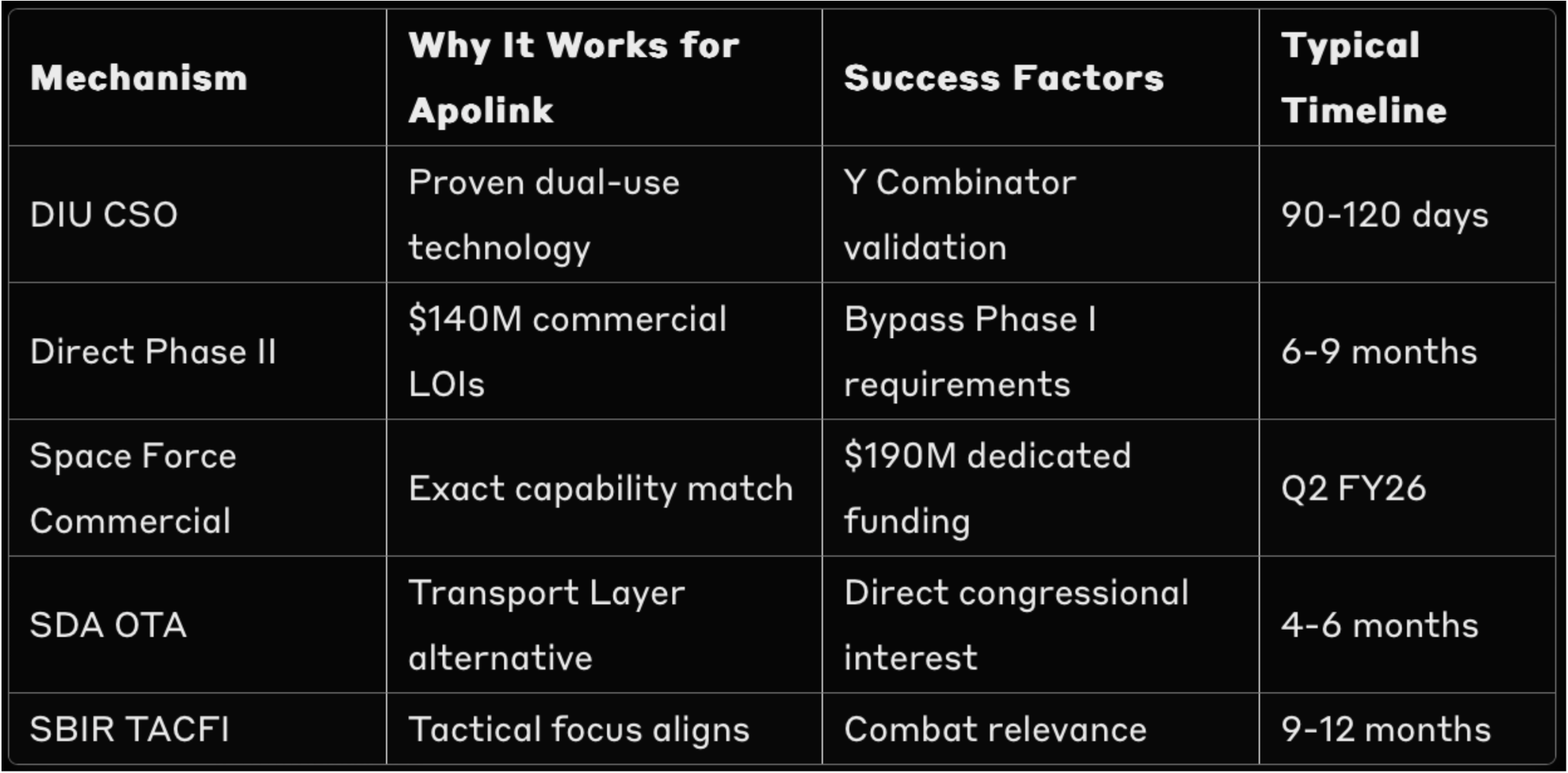

Skip Phase I, Go Direct to Phase II: With proven commercial traction and Letters of Intent, Apolink can leverage Direct Phase II SBIR applications, immediately accessing $1.65M awards. The Space Development Agency's explicit need for commercial alternatives makes this particularly viable.

DIU Commercial Solutions Opening: Apolink is perfectly positioned for DIU's CSO process, which can deliver $1-5M prototype contracts in 60-90 days. Their dual-use technology which serves both commercial and defense satellites fits the CSO criteria.

Space Force Commercial Services: The new $190M FY26 budget line for commercial LEO SATCOM services creates a direct procurement pathway without traditional competition gates.

Strategic Entry Points

Matching procurement vehicles to Apolink's current stage

💼 BD Team Focus: The DIU CSO pathway offers the fastest route to contract, but requires polished pitch materials emphasizing dual-use applications. Your $140M in LOIs becomes crucial evidence of commercial viability.

Why This Matters: Traditional federal playbooks create 3-5 year paths to meaningful revenue. Apolink's unique position (venture funding plus commercial validation plus urgent DoD need) enables compression to 12-18 months. The SDA's cancelled Transport Layer and explicit congressional funding for commercial LEO services create unprecedented entry windows. While competitors spend 18 months in Phase I purgatory, Apolink can pursue operational contracts immediately.

Ways to Leverage This:

Submit Direct Phase II SBIR application referencing $140M LOI validation

Engage DIU immediately with emphasis on hardware-independent architecture

Build relationships with SDA leadership actively seeking Transport Layer alternatives

Position for Q2 FY26 when commercial LEO SATCOM funds become available

Document every metric from commercial deployments for sole-source justifications

2️⃣ Budget Intelligence Foundations

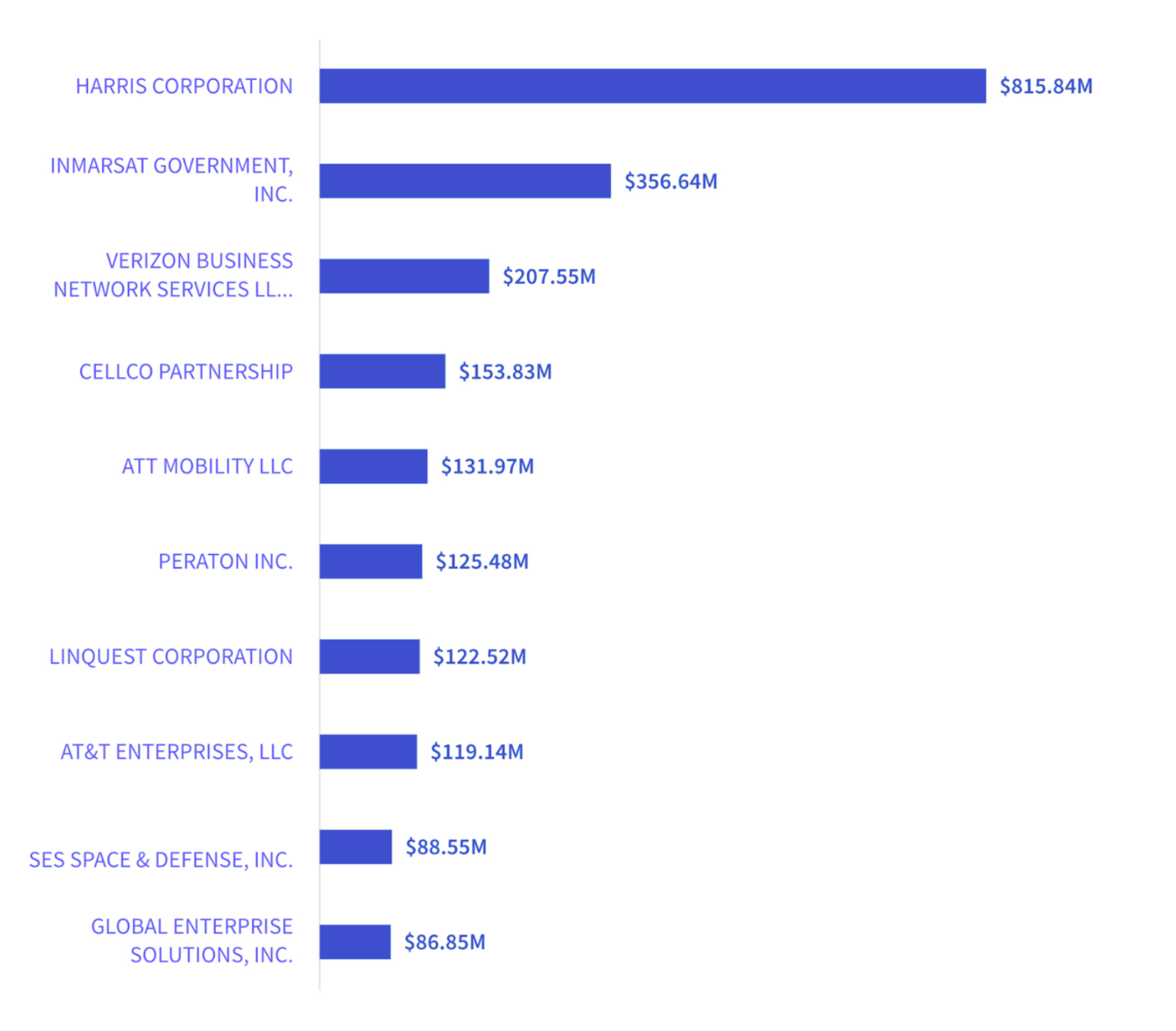

Contractor Landscape Analysis

Who's Winning Today's SATCOM Contracts

The fragmented contractor base reveals no dominant player controls the market. This extreme fragmentation, with the top contractor capturing less than 25% share occurs because each vendor serves narrow niches. None provides the universal LEO connectivity Apolink offers.

💰 How This $3.32B Market Gets Funded:

Congressional Authorization: Defense committees approved $3.66B for Space Force procurement including explicit commercial SATCOM allocations

Appropriation: Funds flow through Defense base budget plus supplementals for Ukraine/Indo-Pacific preparedness

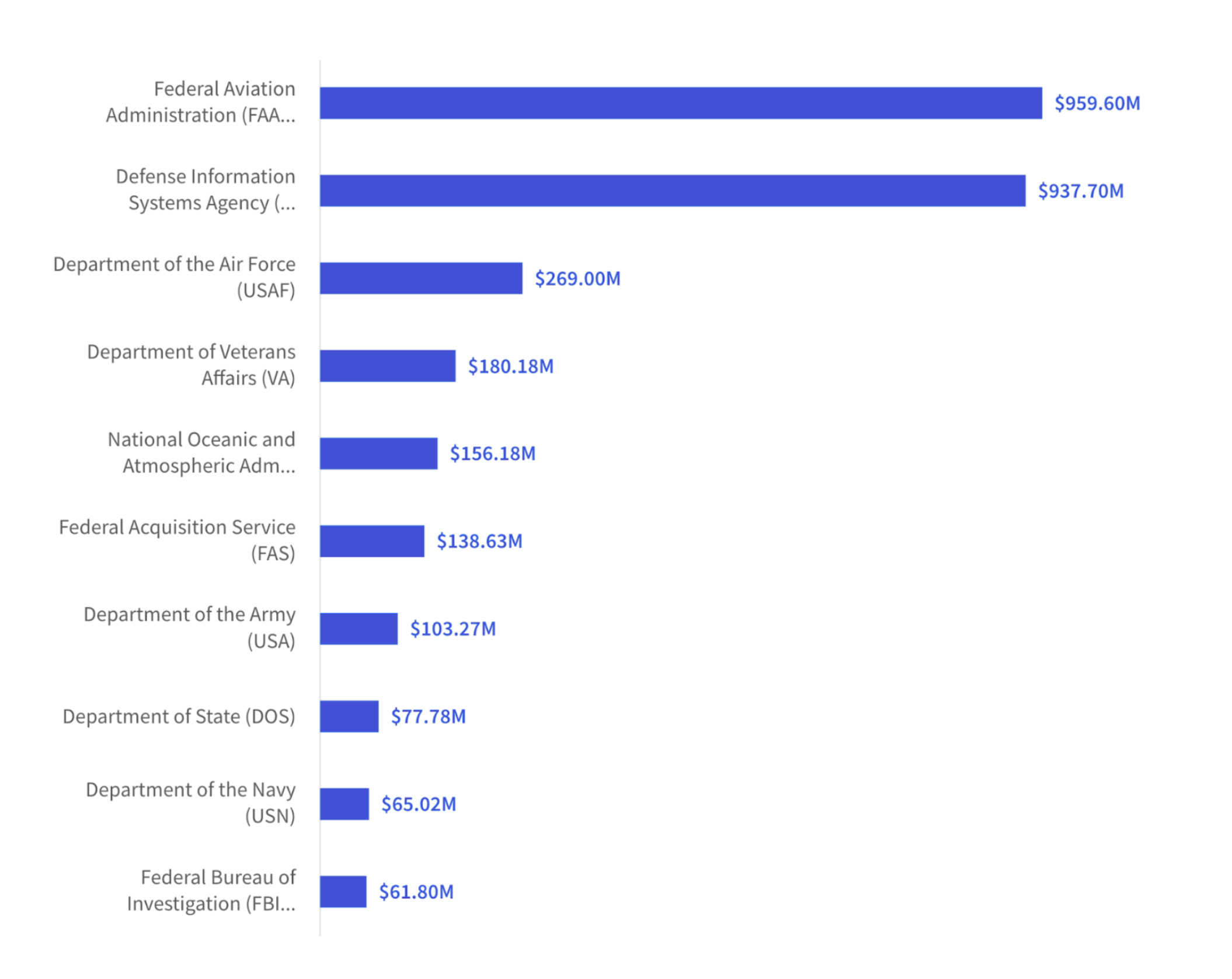

Program Offices: Money allocated to Space Systems Command ($1.2B), DISA ($937M), and service-specific SATCOM offices

Contract Vehicles: Executed via DISA Encore III (45%), GSA Schedules (30%), and full-and-open competition (25%)

Award Timing: Based on patterns, expect 68% obligation by Q3 with September surge

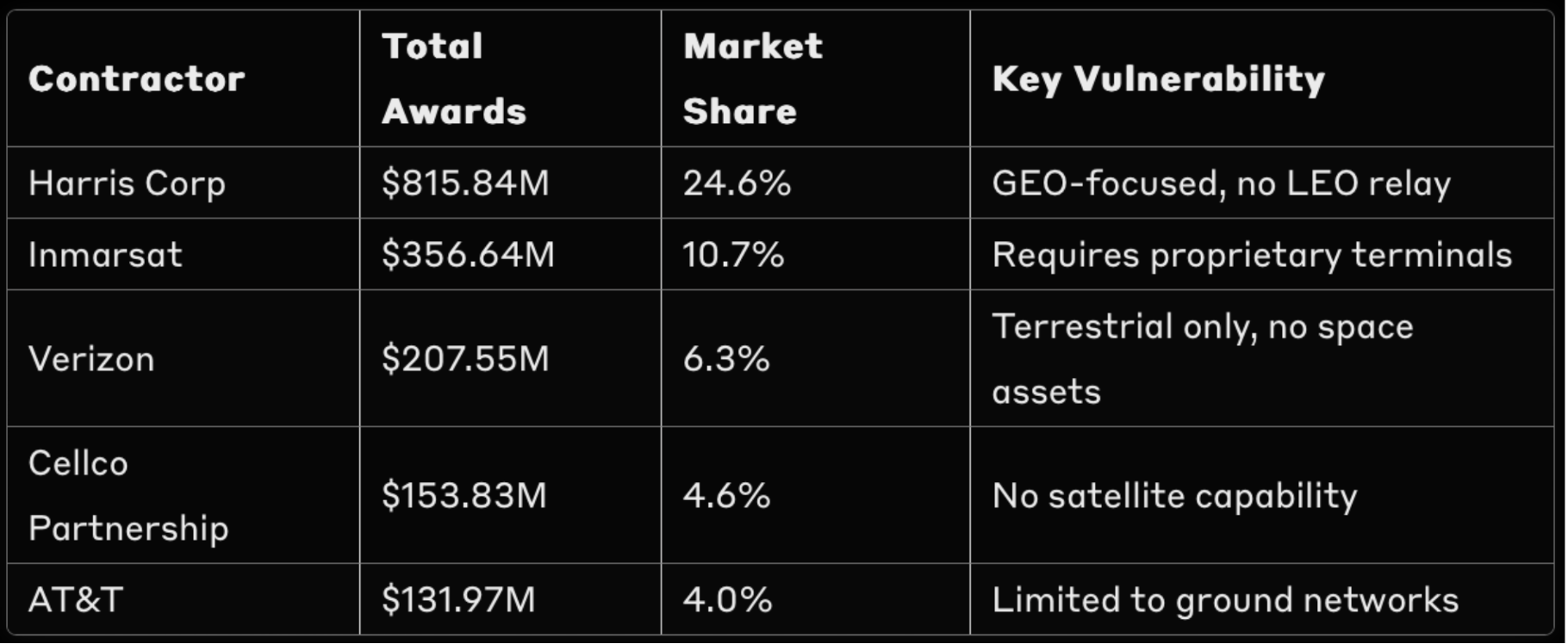

Contractor Analysis

Analyzing market leaders reveals critical vulnerabilities

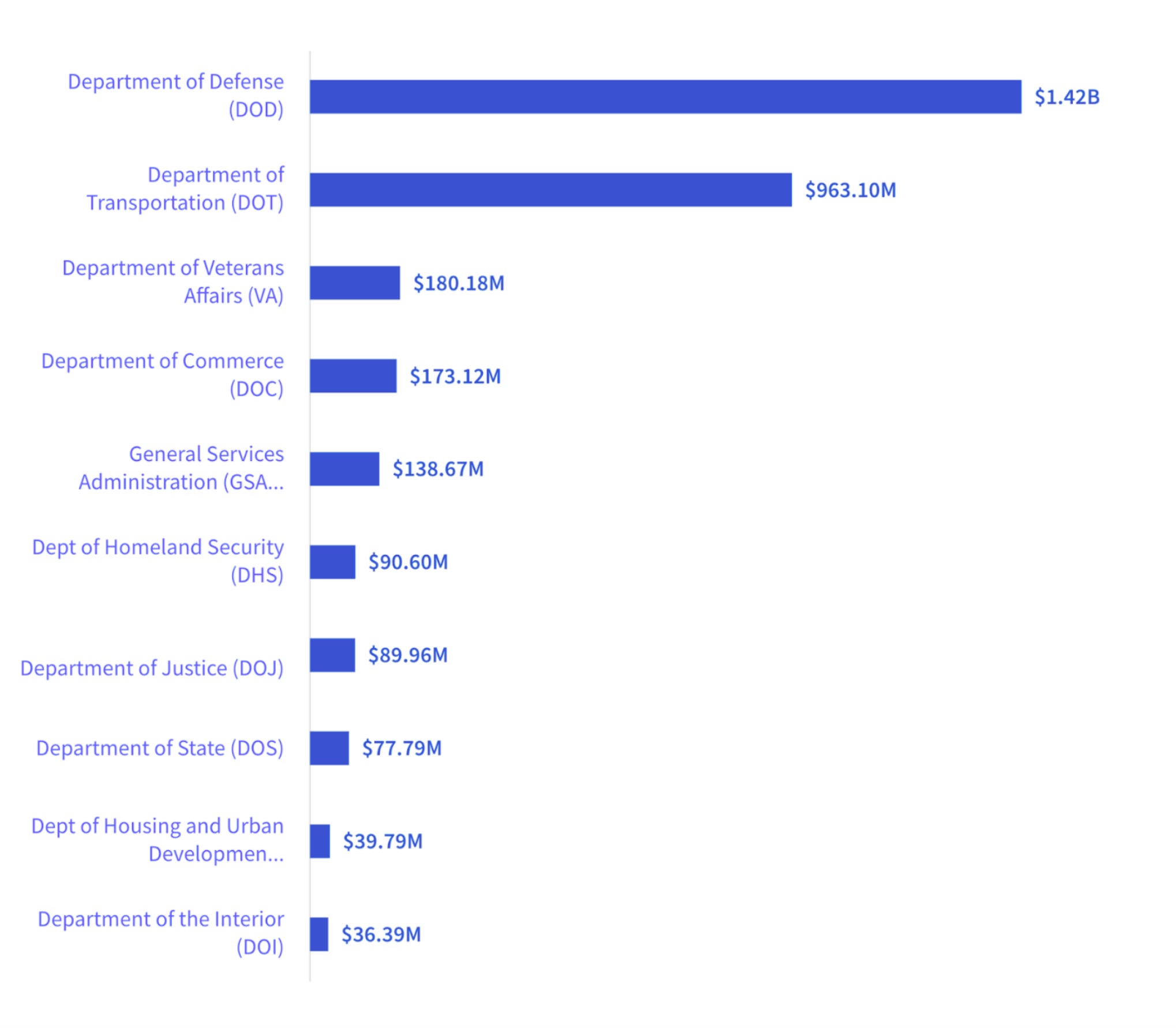

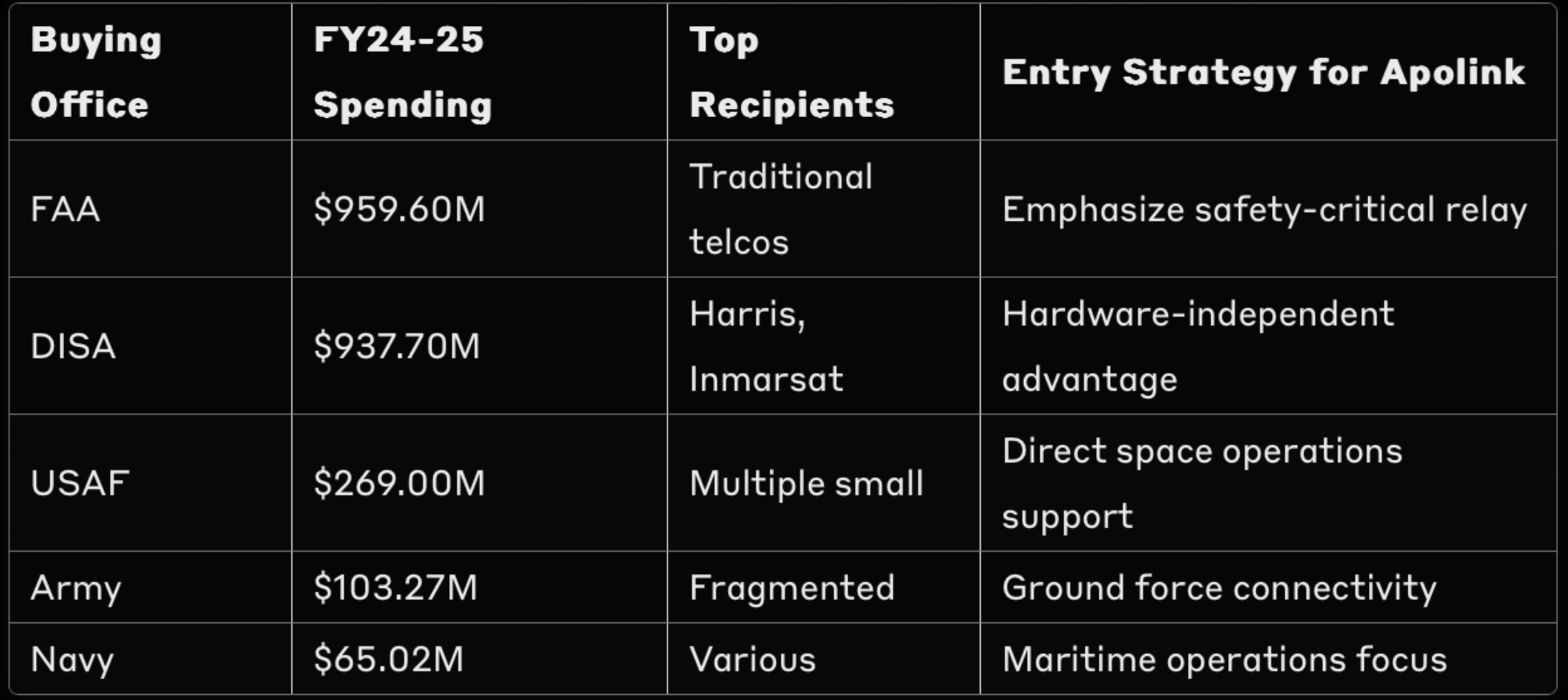

Federal Agency Spending Distribution

Following the Money Through Agency Budgets

Understanding which agencies control satellite communications budgets reveals multiple entry points beyond traditional DoD channels. The significant spending by civilian agencies like DOT and DOC represents untapped opportunities for dual-use technologies.

Subagency Opportunities

Strategic entry points for Apolink's capabilities

🎯 Capture Team Alert: DISA's dominance with nearly $1B in spending but reliance on legacy vendors creates a massive disruption opportunity. Their next-generation requirements explicitly call for interoperability, Apolink's core strength.

Why This Matters: Market fragmentation is Apolink's friend. No entrenched monopoly exists in LEO relay services because the capability barely exists today. The largest contractors remain locked into legacy GEO systems requiring expensive ground terminals. Apolink's plug-and-play approach to existing satellites creates an entirely new market category. The top 10 contractors combined capture less than 50% of spend. This is significant fragmentation for a mature market occurs because agencies buy custom solutions for unique requirements.

Ways to Leverage This:

Target DISA's next-generation SATCOM requirements emphasizing interoperability

Position for FAA's aviation safety communications highlighting global coverage

Emphasize cost savings versus Harris/Inmarsat proprietary systems

Build simultaneous relationships across all major buying offices

Frame capabilities as creating new category rather than competing in existing ones

3️⃣ Pre-Solicitation Monitoring

Active Opportunities Shape Future Requirements

Your 6-Month Window to Influence Procurement

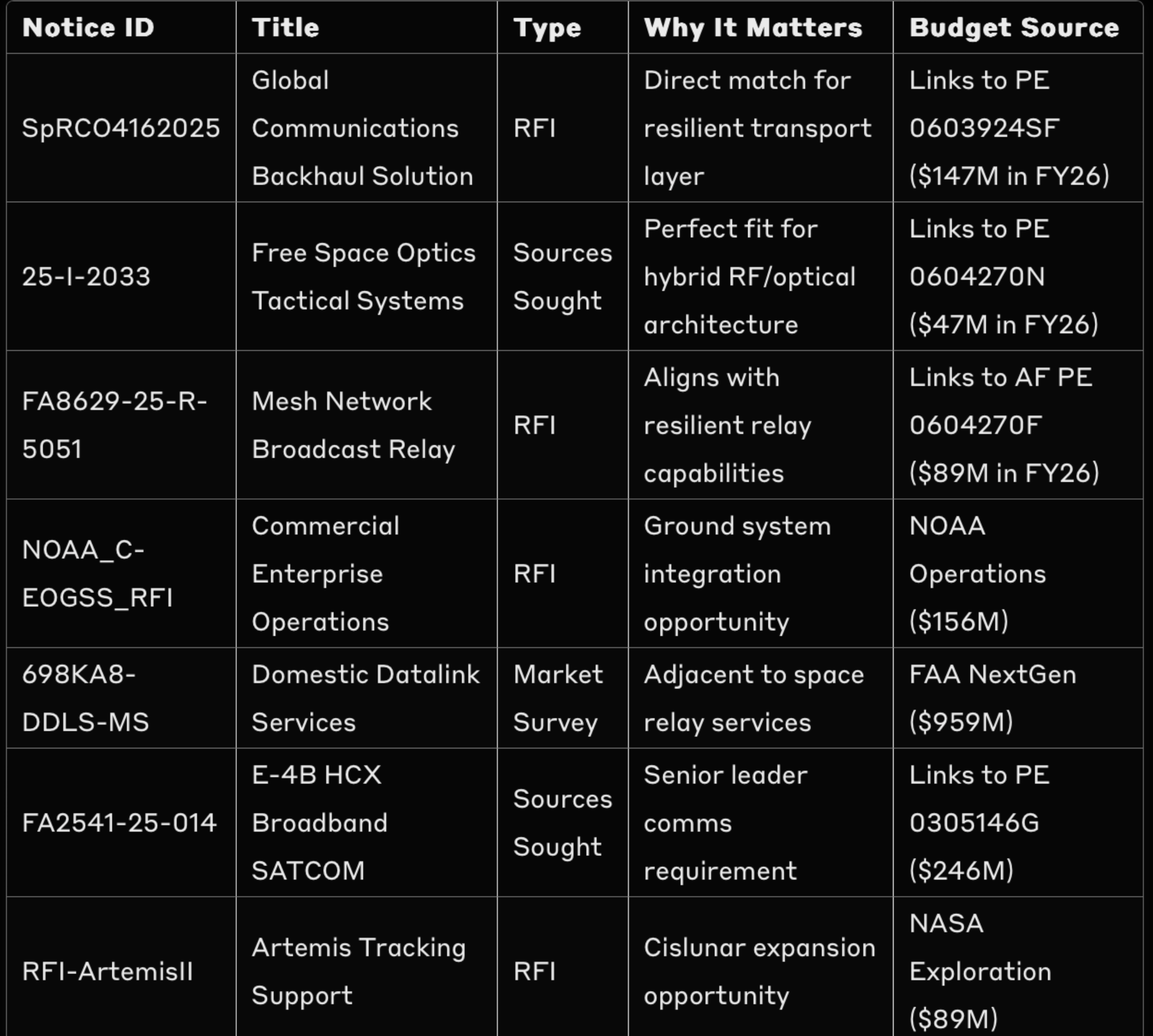

Note: These opportunities represent a snapshot of active requirements as of September 2025. Always verify current status on SAM.gov before responding.

Pre-solicitations reveal agencies struggling with identical problems: legacy SATCOM can't support proliferated LEO constellations, existing ISLs lack interoperability, and proprietary terminals create vendor lock-in. Apolink's responses can literally shape evaluation criteria 6-12 months before RFPs drop.

Current Active Opportunities

Priority opportunities requiring immediate response

Requirements Shaping Patterns

Analysis reveals emerging themes:

"Resilient communications" appears in 5 of 7 notices

"Commercial solutions" explicitly requested in all Space Force requirements

"Interoperability" and "open architecture" becoming mandatory

Subscription-based pricing models being tested

Hybrid RF/optical specifically mentioned twice

🔧 Engineering Note: The USMC FSO notice specifically calls for tactical free-space optical systems, a possible match for Apolink's hybrid RF/optical architecture. Engineering should prioritize technical white papers demonstrating this capability.

Why This Matters: Pre-solicitations are where requirements get shaped. Every response Apolink submits helps define the problem around their solution. The explicit requests for hybrid RF/optical systems and hardware-independent approaches suggest someone in government already understands the need for Apolink's exact capability. Sources Sought responses directly influence set-aside determinations, evaluation criteria, and even pricing models 6-12 months before contracts are awarded.

Ways to Leverage This:

Submit comprehensive responses to SpRCO and USMC notices immediately (strongest alignment)

Include $140M LOI validation as evidence of commercial viability

Propose performance metrics that favor plug-and-play architectures

Emphasize unique 99% uptime capability in all responses

Request one-on-one industry days to demonstrate technology

4️⃣ Capability Alignment

Translating Innovation into Procurement Language

From Silicon Valley Innovation to Pentagon Requirements

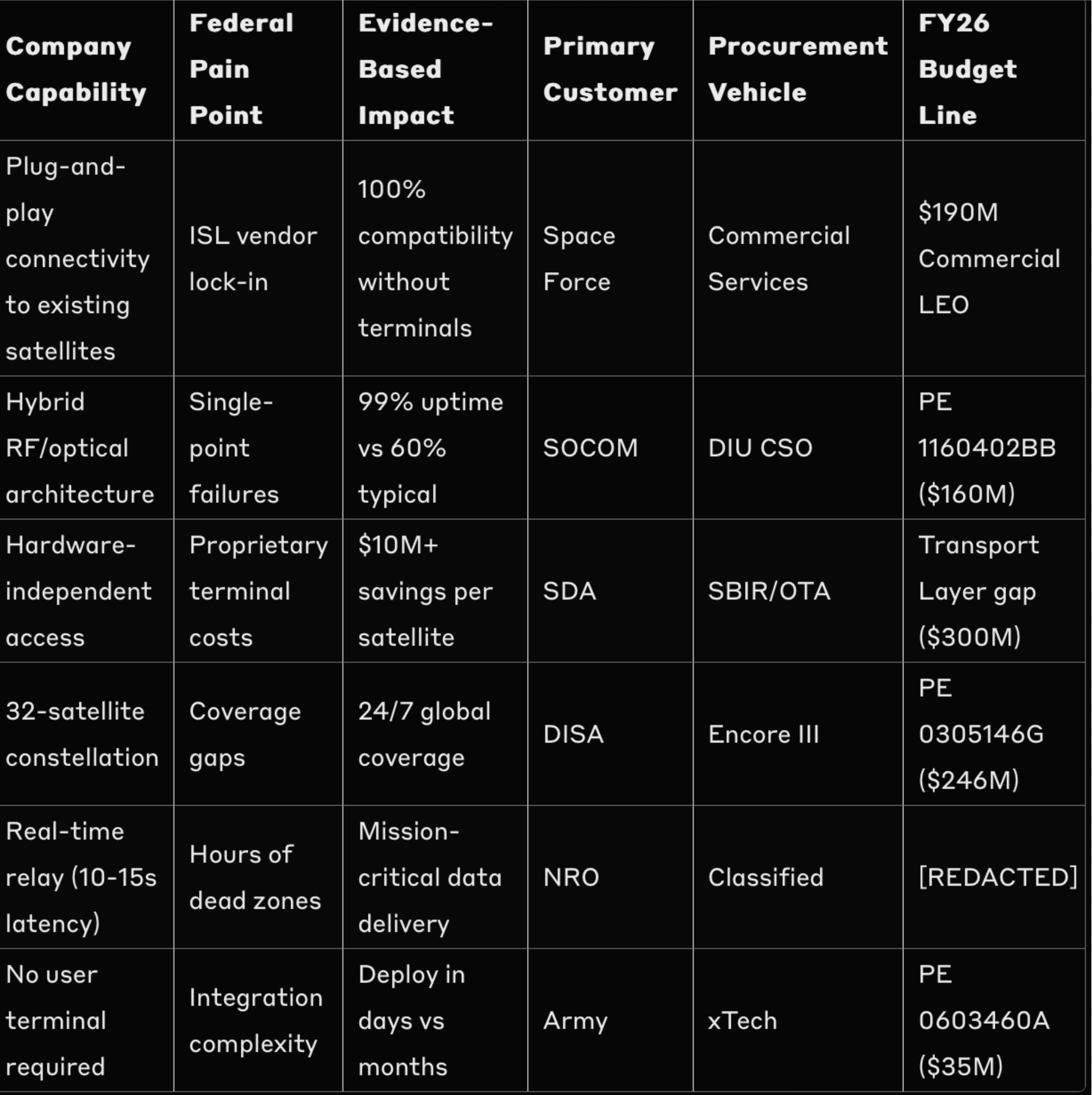

The most sophisticated technology fails if it doesn't translate into procurement language. Here's how Apolink's capabilities map to funded requirements:

Contract Vehicle Alignment

💡 Product Team Insight: Federal evaluators score "mission impact" highest. Frame every feature through operational outcomes: "99% uptime" becomes "zero missed intelligence windows." "Hardware-independent" becomes "deploy to any satellite in 48 hours."

Why This Matters: Apolink's hardware-independent approach solves multiple procurement nightmares simultaneously. Agencies can access the capability without modifying existing satellites, avoid vendor lock-in, and reduce lifecycle costs by millions. This translates directly into evaluation advantages across every procurement vehicle. The ability to provide connectivity without requiring specialized terminals eliminates the single biggest adoption barrier for satellite operators.

Ways to Leverage This:

Create capability briefs for each customer segment emphasizing their specific pain points

Develop TCO models showing 70% cost reduction versus proprietary systems

Map every feature to specific funded requirements in budget documents

Build "plug-and-play" demonstration for congressional staffers

Translate latency improvements into operational advantages (faster targeting, etc.)

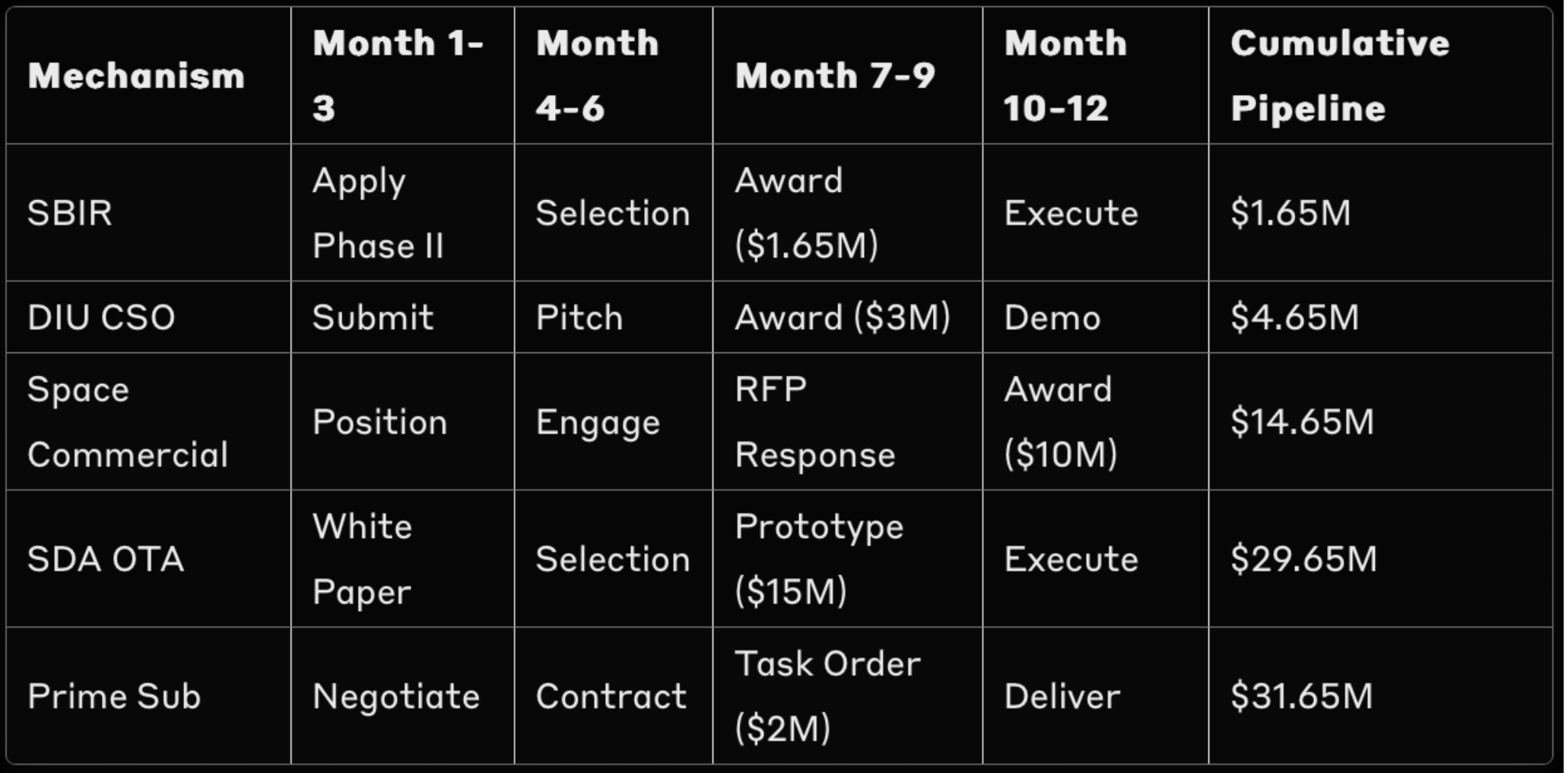

5️⃣ Advanced Opportunity Pipeline

Parallel Pursuit Strategy Accelerates Federal Entry

Building Multiple Pathways to Revenue

Traditional federal playbooks prescribe sequential advancement: SBIR → OTA → Production. Modern defense markets reward companies executing multiple strategies simultaneously. Here's Apolink's parallel pathway approach:

Sprint Paths (3-6 months):

DIU Commercial Solutions: $2-5M for LEO relay demonstration

Direct Phase II SBIR: $1.65M leveraging commercial validation

AFWERX STRATFI: $3M+ with VC matching structure

Space Force pitch days: $750K-1.5M rapid awards

Congressional delegation demos: Position for plus-ups

Scale Paths (6-12 months):

SDA Transport Layer alternative: $15-30M prototype

DISA Encore III on-ramp: Position for 10-year vehicle

Congressional plus-up: Target $25M in FY26 supplemental

International demonstrations: Five Eyes validation

CRADA partnerships: Tech transfer with national labs

Production Paths (12-24 months):

Commercial LEO services contract: $50M+ from $190M allocation

Program of Record integration: Baseline adoption

FMS opportunities: Allied force multiplication

Constellation deployment funding: Mixed commercial/federal

Enterprise blanket purchase agreements: Recurring revenue

Opportunity Stacking Timeline

Total Active Pipeline: $30M+ in 12 months through parallel execution

🎯 Capture Strategy: While competitors chase one opportunity, Apolink should maintain 7+ active pursuits. Historical win rates suggest 30-40% success, but early wins create momentum that improves later odds.

Why This Matters: Parallel pursuit dramatically de-risks federal market entry. While competitors pursue one opportunity at a time, Apolink can manage 7+ simultaneously. Some will fail, but diversification can reduce the risk while maximizing expected value. Early smaller wins provide credibility for larger pursuits. The cumulative pipeline creates momentum that attracts both government attention and investor confidence.

Ways to Leverage This:

Dedicate BD resources to manage 7+ active pursuits simultaneously

Track win/loss factors across all pursuits to improve approach

Use early SBIR/CSO wins as proof points for larger competitions

Stack compatible funding sources for same technology development

Build prime partnerships while pursuing direct awards

6️⃣ FY26 Forward-Looking Budget Intelligence

Congressional Mandates Create LEO Revolution

Following the Money from Authorization to Award

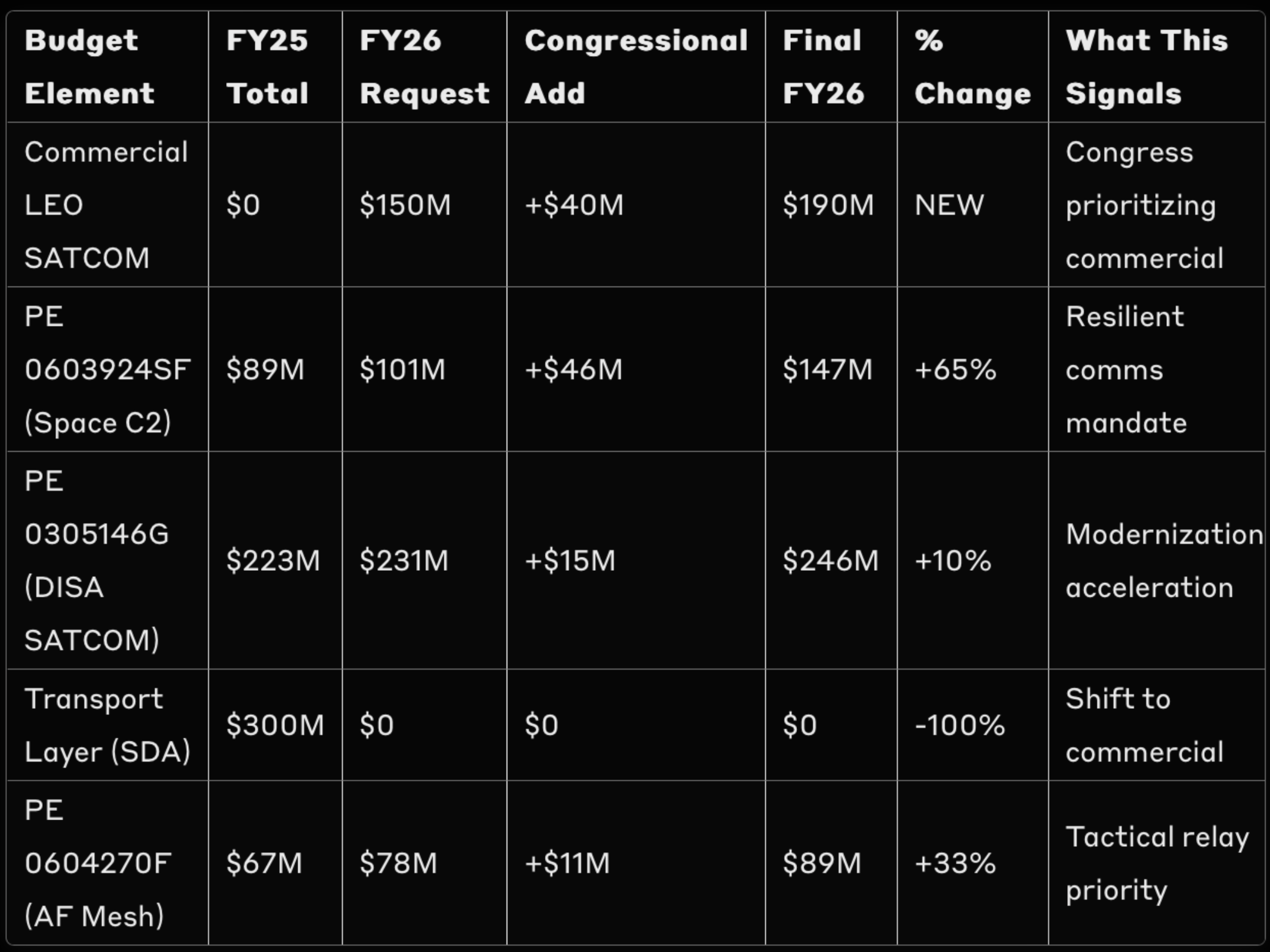

Analysis of FY26 budget documents reveals dramatic shifts in space communications funding. Not random increases, but targeted investments addressing specific capability gaps that Apolink directly fills.

Budget Growth Analysis

📊 Following PE 0603924SF from Budget to Contract:

Congressional Justification: "Develop resilient, proliferated communications leveraging commercial innovation"

Historical Obligation Rate: 72% typically obligated by Q3

Prior Year Execution: $67M to traditional contractors, $22M to new entrants

Contract Vehicle History: 45% OTA, 35% CSO, 20% SBIR

Apolink Positioning: Direct alignment with "commercial innovation" mandate

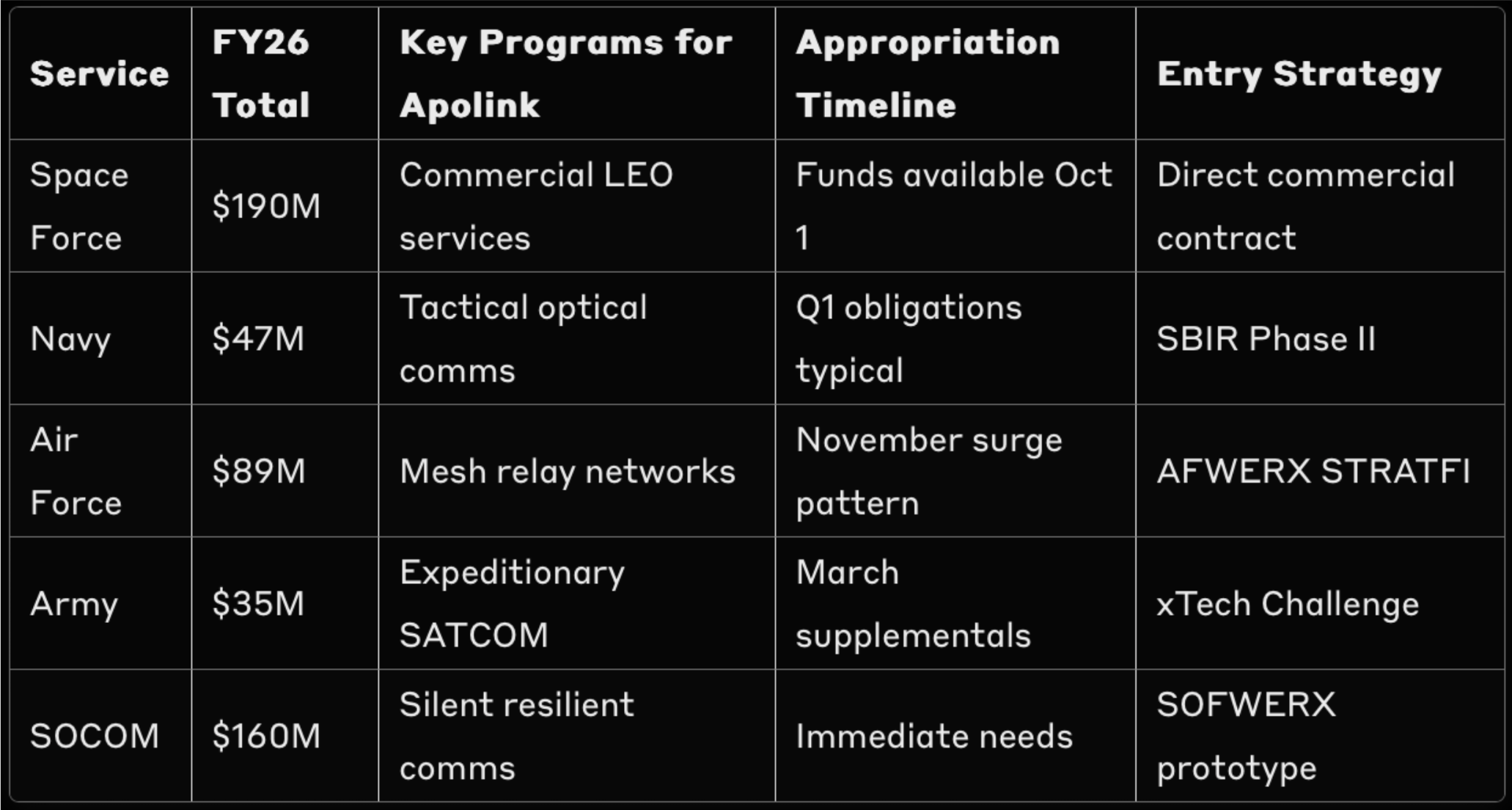

Service-Specific Opportunities

⏰ Key Appropriations Dates for Apolink:

September 2025: Conference committee finalizes FY26 (watch LEO plus-ups)

October 1, 2025: FY26 funds available for obligation

November 2025: Historical surge in SATCOM contracts (31% of annual)

January 2026: Supplemental discussions begin (Ukraine/Taiwan)

March 2026: Mid-year execution reviews drive requirement modifications

Critical Budget Themes

1. Commercial-First Mandate: Explicit congressional language preferring commercial solutions over government-owned systems

2. Resilience Requirements: Every program emphasizes anti-jam, anti-spoof, and redundant communications

3. Interoperability Focus: Open architecture and hardware-independent solutions becoming mandatory

💰 Appropriations Intelligence: The 65% increase in Space C2 funding didn't emerge from Service requests, it's a Congressional add driven by combatant commander unfunded priority lists. Translation: operators desperately want this capability and went around bureaucracy to get it.

Why This Matters: The convergence of dedicated funding ($190M), capability gaps (SDA Transport Layer), and congressional mandates creates a generational opportunity. Traditional contractors can't pivot their proprietary systems fast enough. While they protect yesterday's revenue, an entirely new market for hardware-independent LEO connectivity emerges. The window for establishing category leadership closes within 18-24 months as these funds get obligated.

Ways to Leverage This:

Reference specific PE codes and congressional language in every proposal

Time all major submissions for October-November FY26 obligation surge

Build relationships with House Strategic Forces Subcommittee staff

Frame all capabilities using exact budget document terminology

Track obligation rates monthly to identify when funds become available

🎯 To Wrap Up

Three key standouts from this week’s deep dive into Apolink's federal opportunity:

First, timing creates competitive advantage. The $190M FY26 allocation for commercial LEO SATCOM services isn't incremental funding, it's Congress forcing transformation. Combined with SDA's cancelled $300M Transport Layer, this creates a half-billion-dollar vacuum that traditional contractors can't fill with their proprietary, terminal-dependent systems.

Second, hardware independence wins the procurement war. While SpaceX Starlink requires optical terminals and Amazon Kuiper builds closed ecosystems, Apolink's plug-and-play connectivity to any existing satellite solves the interoperability nightmare plaguing DoD. This isn't just technical superiority, it's procurement genius that eliminates adoption barriers.

Third, commercial validation accelerates federal adoption. Apolink's $140M in LOIs transforms them from speculative startup to validated solution provider. This enables Direct Phase II SBIRs, DIU fast-track awards, and positions them as the obvious choice for the commercial LEO services contract.

The hidden leverage point nobody discusses: The satellite communications market fragments across dozens of incompatible systems because no universal standard exists. Apolink is providing more than connectivity, they're creating the interoperability layer that enables the entire proliferated LEO ecosystem. Master this narrative, and they don't just win contracts, they become infrastructure.

Next Moves:

✅ This Week: Submit comprehensive responses to SpRCO Global Communications Backhaul (due Sep 30) and USMC Free Space Optics notices, review House Armed Services report language on commercial SATCOM priorities

✅ Next 30 Days: Prepare Direct Phase II SBIR application emphasizing $140M commercial validation, engage SDA leadership on Transport Layer alternatives, schedule demonstrations for key congressional staff

✅ Next Quarter: Position for Q2 FY26 commercial LEO services RFP, establish prime partnerships for vehicle access, align with FY27 POM cycle for sustained funding

🏗️ Building This Playbook Together

I would love to hear your feedback. Are there specific NAICS codes/PSCs or procurement challenges you're wrestling with? My goal here is to provide tactical, actionable insights that you can implement immediately. I'm actively working through these same challenges in the industry and view this newsletter as a collaborative effort to build better structured approaches to federal markets.

This methodology evolves with every conversation. The framework you're reading has been shaped by discussions with founders, investors, and operators. Your feedback directly influences next week's analysis.

I don't just analyze where contracts land, I trace the money from congressional authorization through appropriation to obligation. This helps you see opportunities 6-12 months before RFPs drop.

Each week, I'm revealing new patterns and opportunities hidden in public data. But the real value comes from applying these insights to your specific situation.

Is there a VC-backed defense startup you'd like to see featured? Drop me a note.

Connect with me:

in

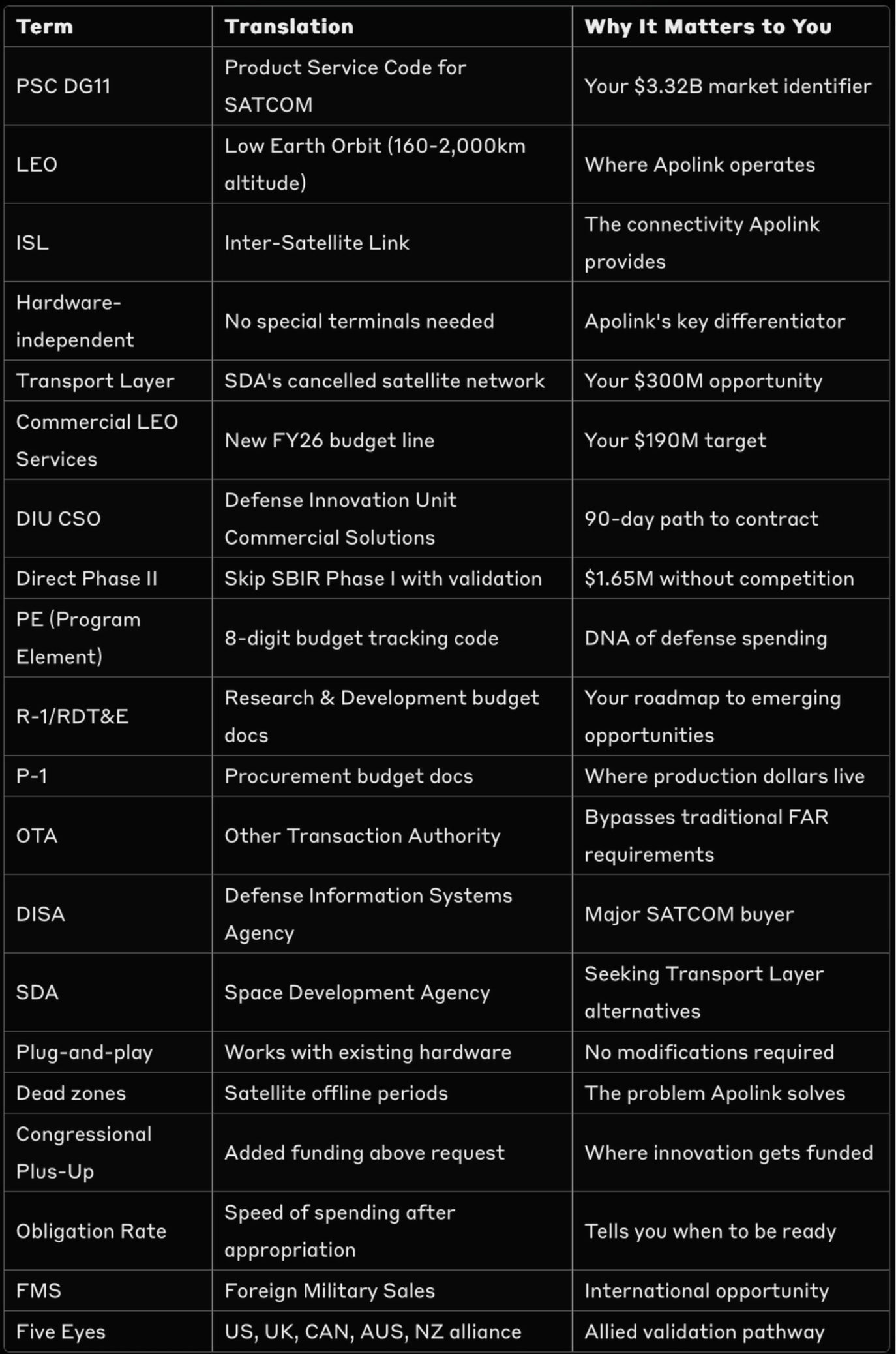

Descrambling This Week's Jargon

Next week: Another VC-backed defense startup paired with their PSC/NAICS code. Same systematic approach, new market insights. Reply with suggestions!

Data current as of September 6, 2025. Analysis based on USAspending.gov PSC DG11 obligations filtered for "Satellite" and "Relay" keywords for FY24-25 (through latest reported data, which typically lags 30-90 days), SAM.gov active opportunities, and FY26 defense budget documents: DISA_OP-5, RDTEN_BA4_Book (5), RDTEN_BA6_Book (4), RDTE_SOCOM_PB_2026 (2), RDTE_Vol1_DARPA_MasterJustificationBook

My analysis traces federal spending from congressional appropriation through contract award, revealing patterns most miss.