FILE 30: FOREIGN BUDGETS UNLOCKED

Breaking down international defense budgets into pursuable opportunities.

Allied governments publish enough award, solicitation, and budget data to support the same analysis that mirrors how the below three-layer framework applies her in the U.S. (see FILE 29). The snapshot below shows the scale of what that opens up.

A note on scope. This framework answers where allied defense money sits and how to read it. What it does not yet answer is whether a company can reach that money, and through which route, entry pathways, TRL thresholds, regime type by market, and the prime-and-consortia layer most startups actually enter through rather than winning direct awards. My foundation is the U.S. system; the allied application is newer ground I'm building out, and several readers already working inside these programs have sharpened it. The access layer, a pre-filter and post-filter wrapped around the core three, is the next edition. If you operate inside these markets and see what the public record cannot, that input is the most valuable thing I can get.

Snapshot Overview

This edition takes the three-layer process used on the U.S. side and runs it against allied procurement systems. The data exists, and in the core allied markets it runs deeper than most teams assume.

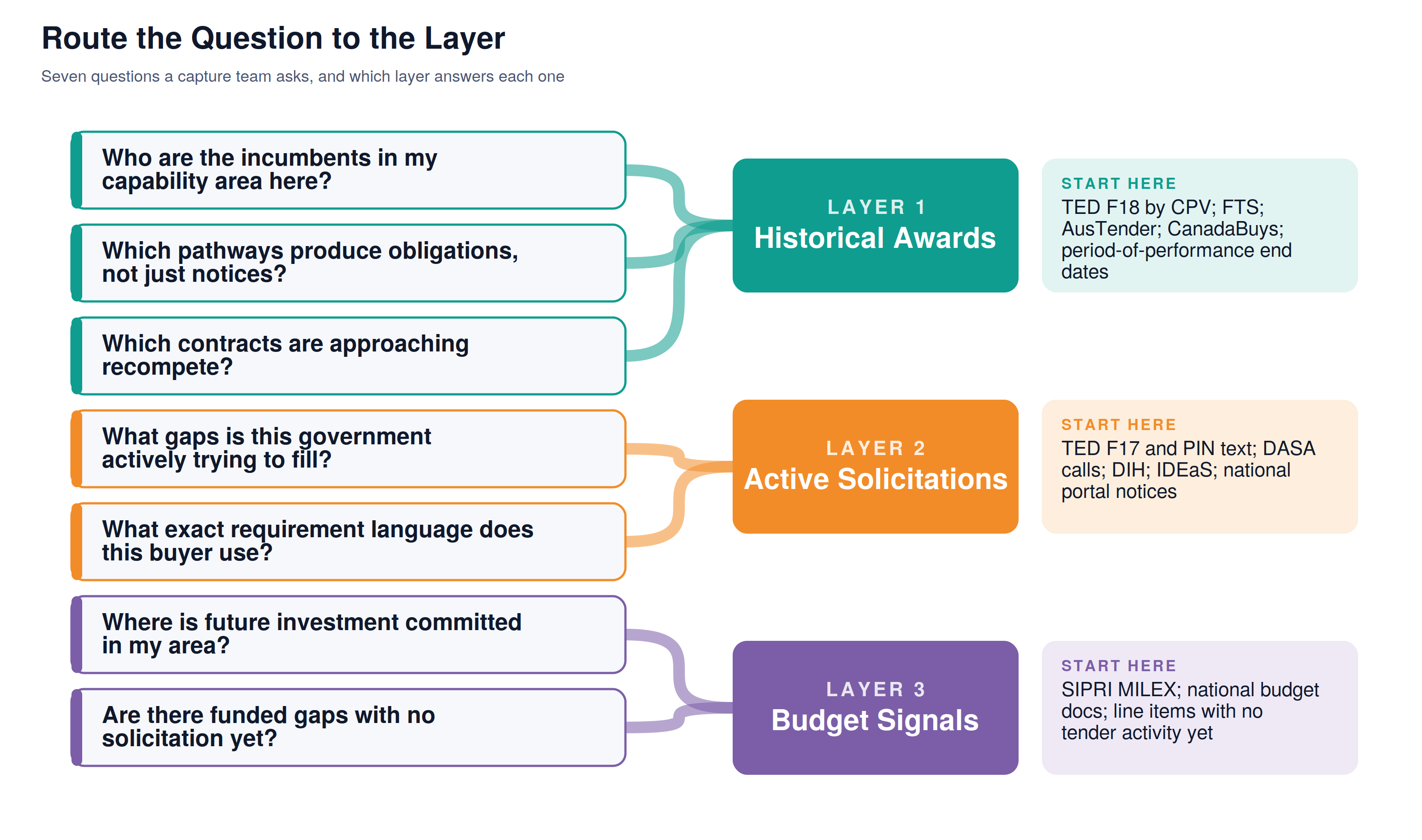

Layer 1: Historical Awards

What allied governments have actually bought and from whom, drawn from award records that run decadeFs deep in the core markets, and how to build a recompete calendar from that data the same way a U.S. capture team tracks period-of-performance end dates.

Layer 2: Active Solicitations

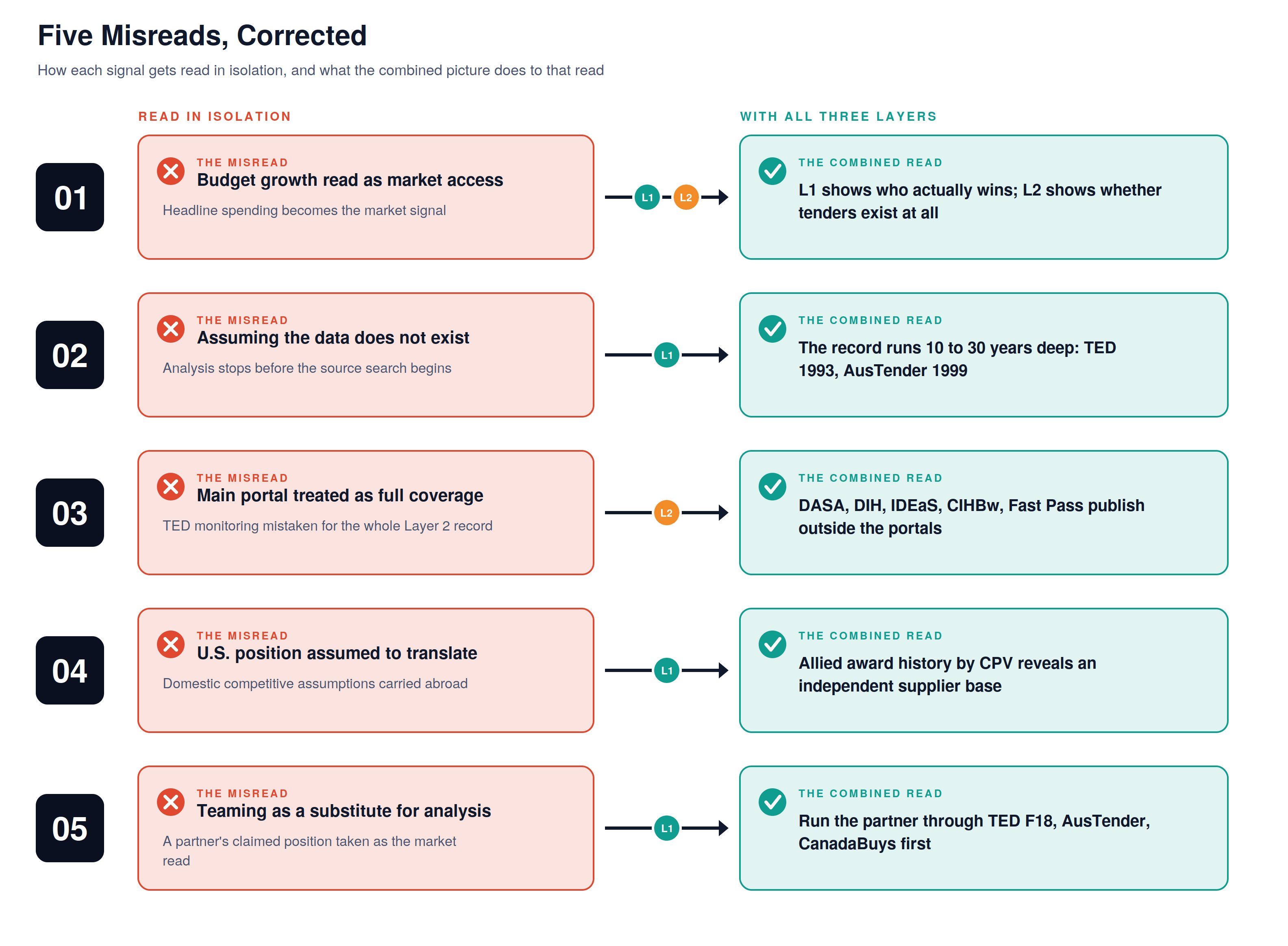

What capability gaps are being shopped right now, in the buyer’s own requirement language, including the innovation pathways (DASA, the Defence Innovation Hub, IDEaS, CIHBw, ATLA Fast Pass) that publish outside the main portals and create the same blind spot as a SAM.gov-only read.

Layer 3: Budget Signals

Where money is committed before any solicitation posts, read from SIPRI, NATO expenditure data, and the national budget documents themselves, with every figure labeled by source type and time horizon.

Wrapped around the three layers: the source discipline (every signal traces to an official record or is labeled as media-sourced), the access layer (FMS, NSPA, treaties, offsets, and the export controls that decide whether intelligence becomes a viable pursuit), and the working applications, which functions use which layer and the five patterns that show up when any single signal gets read alone.

Who This Serves

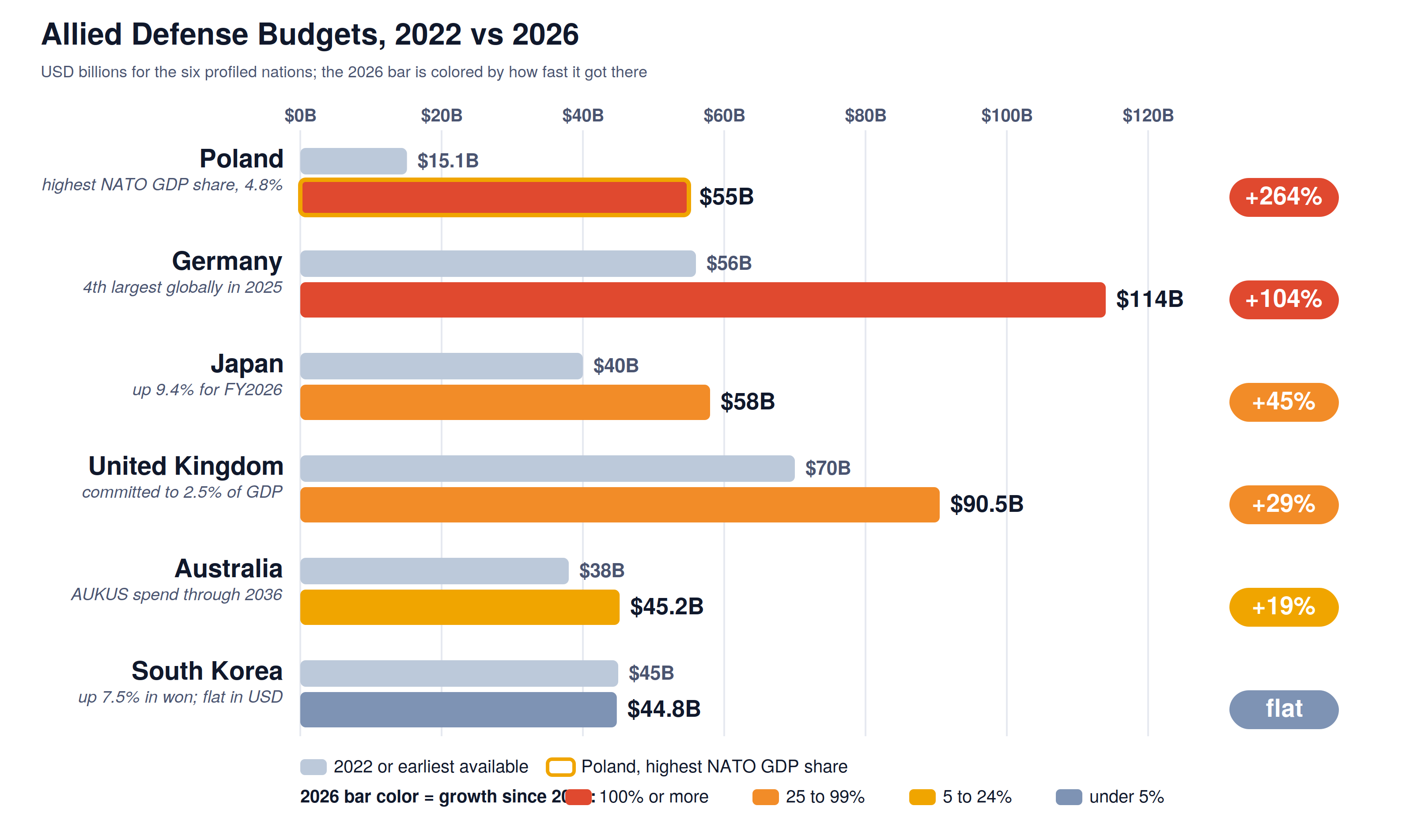

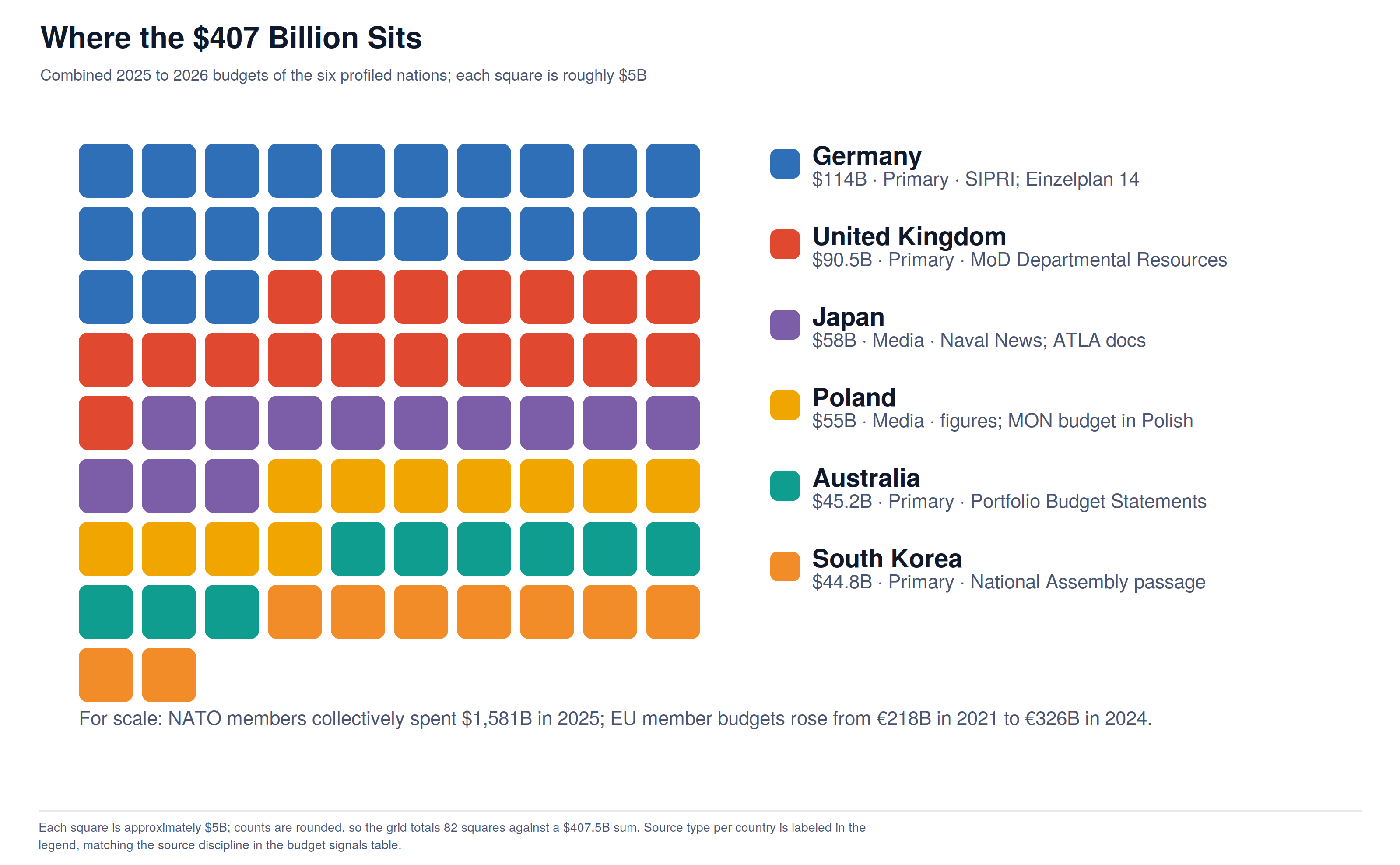

Allied defense markets are not a niche add-on to a U.S.-first strategy. At a time when NATO members collectively spent $1,581 billion on defense in 2025, when Poland’s defense budget jumped from $15.1 billion in 2022 to $55 billion in 2026, and when Australia is committed to between $50.7 billion and $68.6 billion USD in AUKUS-related spending through 2036, the scale of accessible procurement opportunity outside the U.S. system is real enough to warrant the same analytical discipline.

This edition serves any team weighing an allied market against pursuit resources. That includes BD and capture teams qualifying whether international opportunities are structurally accessible in their capability area, early and growth-stage startups reading which pathways admit new entrants, commercial companies mapping defense as a new buyer, established contractors and primes looking past their existing program relationships, and the leadership and strategy functions that need an auditable, evidence-grounded basis for entry, resource, and partnership decisions. The roles differ. The requirement does not: the same source discipline applied internationally that these teams already run at home.

Framework and Important Note

The framework used in this report is the same one I use to map U.S. defense markets: triangulate across three time horizons using distinct primary sources at each layer. Historical award records show what a government has actually bought. Active solicitations show what they are buying now. Forward budget documents show where money is committed to flow next. The layers stay separate. A historical award is not a proxy for current demand. A budget signal is not treated as near-term revenue. Each one answers a different question, and the value of the combined picture comes from reading all three together.

The difference is the subject: allied and partner nations operating outside the U.S. procurement system. The central question I worked through before writing this is whether enough publicly available data exists in those foreign systems to run the same process. The answer is yes for a meaningful subset of allied nations, and the data is structured, machine-readable, and in several cases API-accessible. Where it is not available or not verifiable, I say so.

Important Note: This is my interpretation of the opportunity and the data infrastructure around it. Many companies are already operating in international defense markets with strategies I cannot see from the outside. Others are evaluating the entry question for the first time. My goal is to present what the public record shows in a transparent enough form that any company, regardless of where they are in that process, can use this as a foundation for their own analysis.

A note on sourcing: Several budget figures are sourced from defense media rather than official government documents because the primary budget documents are either in a foreign language or the specific figures have not yet been published in an English-language official source. Those figures are labeled as media-sourced in the Layer 3 table. The official primary document links are included alongside them so readers can verify directly.

The Opportunity in the Data

A common starting point for international defense market exploration is a trade show conversation, a headline about allied spending going up, or an introduction to a foreign official. All three are legitimate entry points. What I found working through this from the outside is that the public data infrastructure available in allied markets is substantially richer than most practitioners expect, and that the same three-layer process that works on the U.S. side can be applied directly once you know where the sources live.

Allied nations, particularly within the Five Eyes, NATO’s European core, and the Indo-Pacific treaty network, have been building procurement transparency infrastructure for years. Some of it now rivals the functional depth of USASpending.gov and SAM.gov in terms of what can be queried, downloaded, and analyzed at the contract level. The question I worked through first is a practical one: which countries publish enough budget, solicitation, and award data in accessible formats to support the same source-grounded analysis we already run on the U.S. side?

The answer matters because the scale of the opportunity is real. When allied defense budgets are growing at the rates documented below, and when the procurement data infrastructure to analyze that spending is publicly available, the analysis itself becomes a real positioning asset.

The macro context:

World military expenditure reached $2,887 billion in 2025, the highest level ever recorded and the 11th consecutive year of growth. Total NATO member spending reached $1,581 billion. European NATO members alone spent $559 billion. By 2025, all 32 NATO Allies were meeting or exceeding the 2% of GDP defense spending baseline for the first time since that target was set in 2014. At the June 2025 NATO Summit in The Hague, Allies committed to a new 3.5% of GDP target for core defense requirements by 2035. Sources: SIPRI Military Expenditure Fact Sheet 2025; NATO Defence Expenditure Commitments Page.

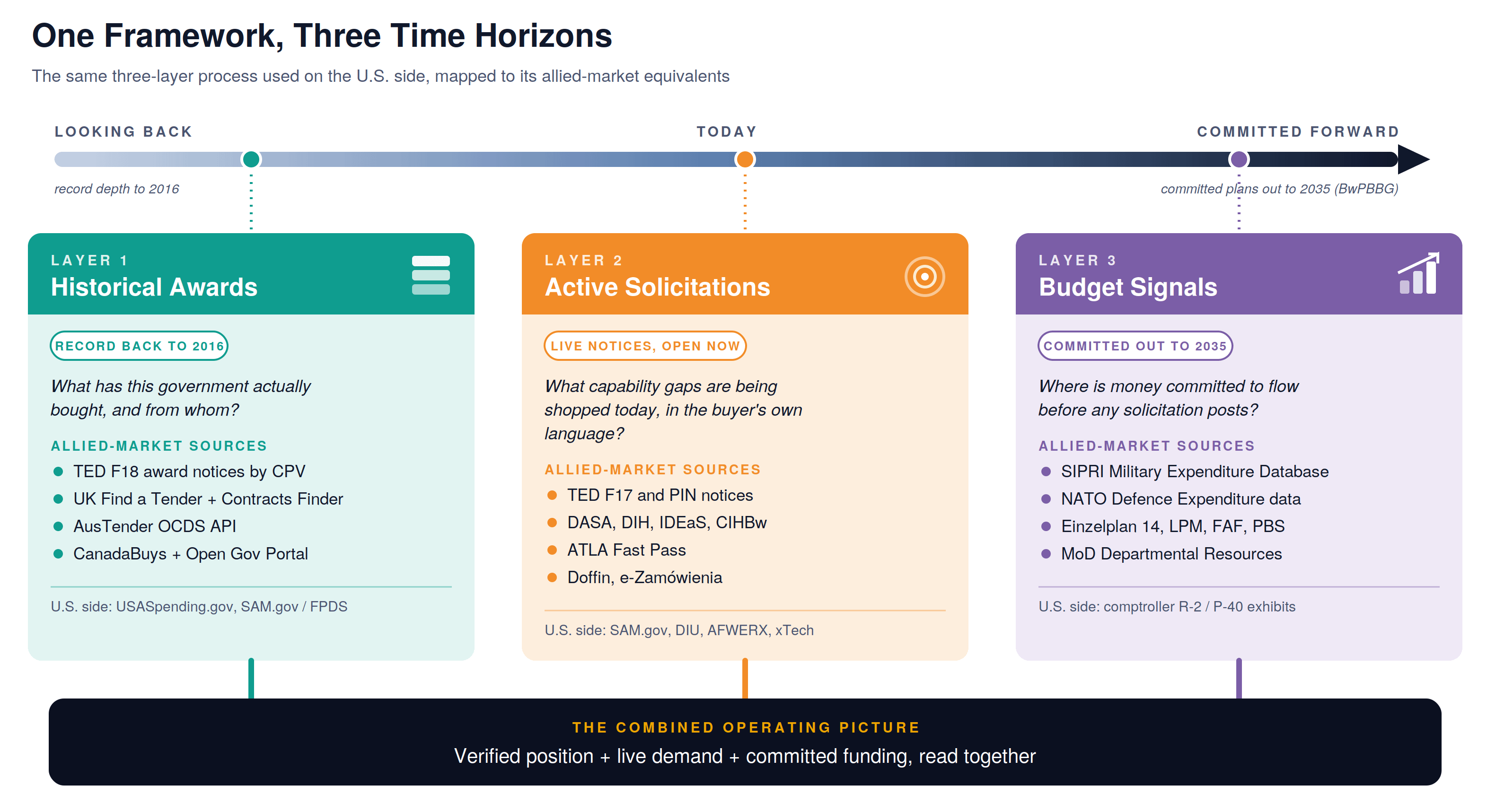

How the Three Layers Map to Foreign Systems

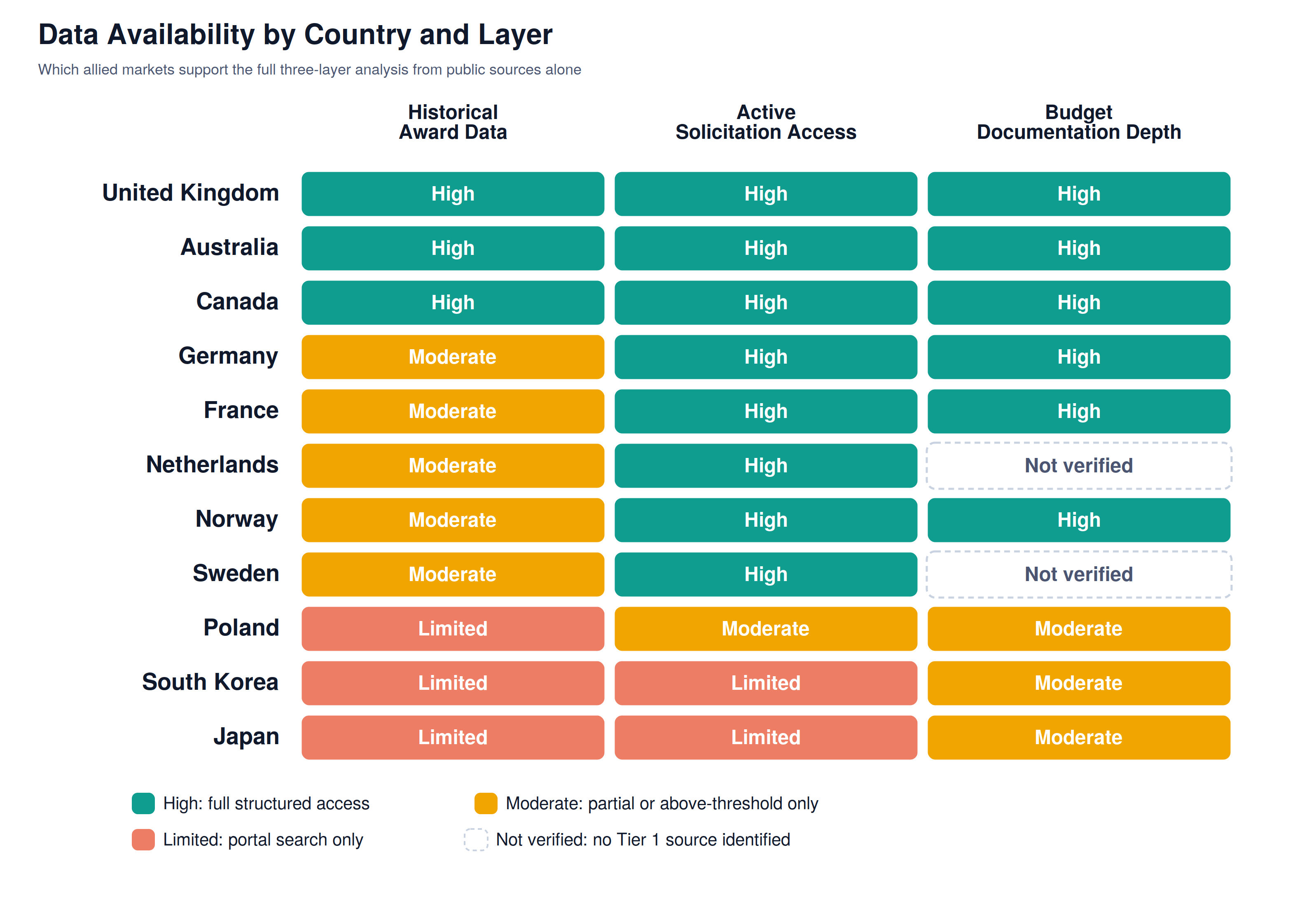

Before going country by country, it is worth naming what the three-layer framework requires at the source level in each foreign system. The layers are identical to the U.S. process. The primary sources are different, and in some markets they are incomplete or partially blocked by national security exemptions. The table below maps the U.S. source set against its international equivalents for the countries where the data density is high enough to support systematic analysis.

Reading the Historical Award Record in Allied Markets

The historical award record is the most evidence-grounded intelligence layer in any defense market. It shows who the government has actually paid, through which acquisition pathways, from which offices, at what dollar volumes, and under what contract structures. Without it, you are navigating the competitive landscape based on what vendors say about themselves, not what the government has actually funded.

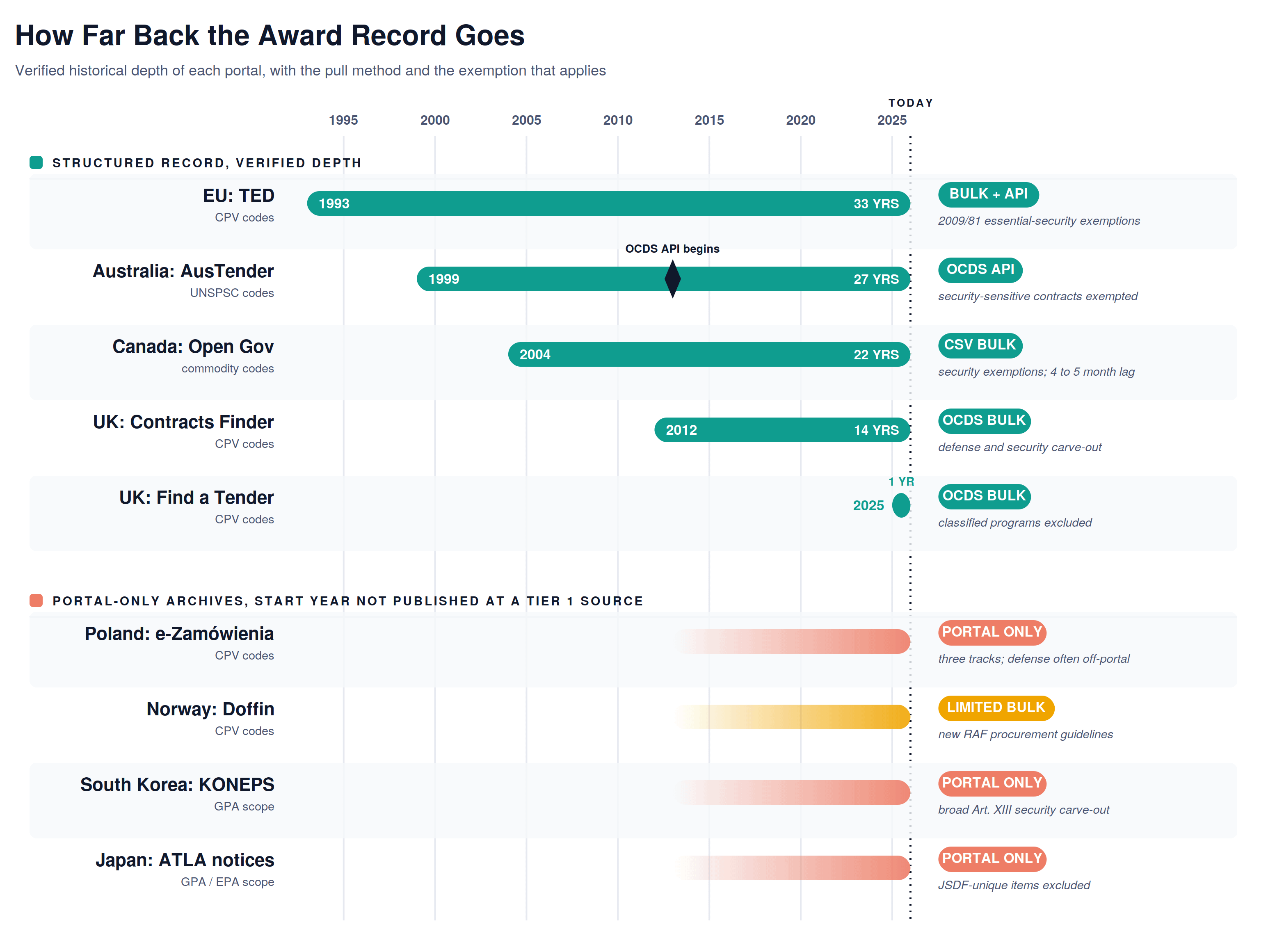

In foreign systems, the award history layer operates on the same logic as USASpending.gov but uses different vocabulary to organize the data. In EU and UK systems, the classification code is the CPV (Common Procurement Vocabulary) rather than NAICS or PSC. Defense-specific CPV codes fall primarily under Chapter 35 (security, defense, and police equipment) and parts of Chapter 98. Querying TED or Find a Tender by CPV code plus notice type F18 (contract award notice) plus a date range returns the same information I pull from a USASpending query: awardee, awarding authority, contract value, period of performance, and the description language. For Australia, the equivalent classification is UNSPSC (United Nations Standard Products and Services Code), and the AusTender OCDS API accepts queries by UNSPSC, agency code, supplier name, and date range, returning structured JSON. For Canada, the Open Government Portal proactive disclosure dataset is queryable by department (Department of National Defence or Public Services and Procurement Canada) and keyword.

One structural difference that matters: national security exemptions work differently in each system. The EU Defense and Security Directive (2009/81/EC) governs what must be published above threshold in EU member states, but it directly carves out contracts where disclosure would damage essential security interests. Germany’s BwPBBG, adopted by the Bundestag on 15 January 2026 and entering into force in February 2026, raised direct-award thresholds and expanded the negotiated procedure without prior publication, meaning some contracts that previously appeared in TED will no longer do so. The thresholds adjusted as of 1 January 2026 are EUR 216,000 for supplies and services. Norway’s new defence procurement guidelines (the RAF, replacing ARF, published 1 January 2026) operate under a public access principle with statutory exemptions for sensitive materiel. Knowing these exemption architectures is as important as knowing the portals.

Poland in the Layer 1 record: Poland’s e-Zamówienia portal (ezamowienia.gov.pl) is the national public procurement system where defense and security contracts above EU thresholds are published, consistent with Poland’s obligations under EU Directive 2009/81/EC. Defense procurement in Poland runs through three parallel tracks: public procurement law (the default, rarely used for major defense acquisitions), Ministry of Defence internal procedures under MON Decision No. 367/MON, and government-to-government (G2G) contracts. The G2G track, which covers many of Poland’s largest recent acquisitions (HIMARS, Abrams tanks, F-35s), does not appear in e-Zamówienia. What does appear are above-threshold competitive tenders and framework agreement awards.

South Korea in the Layer 1 record: South Korea’s KONEPS system (g2b.go.kr) is a fully integrated e-procurement platform covering all public procurement. DAPA (Defense Acquisition Program Administration) publishes defense notices at dapa.go.kr. English-language access to GPA-covered contracts is available via JETRO. The GPA Article XIII national security carve-out is broad, meaning a significant portion of DAPA-managed major acquisition programs do not appear in any public database accessible to foreign firms. What does appear: commercial-off-the-shelf acquisitions, some services contracts, and items within the GPA scope. South Korea’s approved 2026 defense budget is 65.9 trillion won ($44.8 billion USD), up 7.5% from 2025, with $13.6 billion dedicated to capability development spending.

Why This Matters

The award history layer tells you who is actually winning in a given market, not who claims to be positioned. For an allied nation, it tells you which acquisition pathways are producing obligations (above-threshold competitive tenders vs. framework call-offs vs. innovation mechanism awards), which procurement offices are real buyers, and which contracts are approaching their period-of-performance end dates and may be re-competed. That last point matters for BD planning: TED F18 notices and AusTender records both include contract start and end dates. A team that tracks those dates is working from the same recompete calendar discipline that drives U.S. capture planning, applied to allied markets.

Ways To Apply This

Start with CPV code identification for your capability area. Run TED filtered by CPV code, notice type F18, and the country or countries you are targeting. For each qualifying award, capture the awardee, awarding authority, value, period of performance end date, and the description language. For Australia, run the same exercise via AusTender using UNSPSC codes and a Department of Defence agency filter. For Canada, query the Open Government Portal by department code (DND or PSPC) and keyword. For Poland, query e-Zamówienia by CPV code and note that G2G track acquisitions will not appear. The period-of-performance end dates across that record are your recompete calendar. The awardee list is your competitive landscape. The pathway distribution is your entry point map.

Building a Recompete Calendar from International Award Data

A recompete calendar is the practical output of Layer 1 analysis. The reasoning does not depend on the market: award records publish period-of-performance end dates, and a pursuit decision made well ahead of expiration beats one made after the follow-on posts. A review trigger set 18 to 24 months out leaves room to qualify, team, and position before that happens. The international version applies the same logic to TED F18, AusTender, and CanadaBuys records.

The process: for each CPV code relevant to your capability area, query TED F18 awards for your target countries over the past five years. Export to a spreadsheet. For each record, note the contract award date, the stated duration or end date, the awarding authority name, the awardee, and the contract value. Sort by estimated end date. Any contract ending within the next 12 to 24 months is a potential recompete. Layer 2 monitoring for new notices from that same awarding authority in the same CPV category is the signal that the re-competition has launched. That is the same process as watching for a SAM.gov Sources Sought or RFI from a contracting office whose incumbent contract you have been tracking.

One structural note: TED F18 records include a field for “initial estimated value” and sometimes for “contract duration in months.” Not all awards include both, and framework agreements often publish the maximum value rather than actual obligation. The discipline is the same as working with USASpending ceiling values: treat as a ceiling signal, not a guaranteed obligation, and cross-reference against active notices from the same office to understand actual demand pace.

Reading Active Solicitations in Allied Markets

Active solicitations are the most time-sensitive layer and the one where the pathway distribution analysis matters most in international markets. In the U.S. system, I tag every solicitation by notice type because Sources Sought, RFI, RFP, BAA, OTA call, and CSO do not carry the same weight or represent the same stage of government intent. The same discipline applies internationally, and the non-equivalence problem is at least as acute.

In UK and EU/TED systems, the notice type taxonomy is standardized. A Prior Information Notice (PIN or F15) is the European equivalent of a U.S. Sources Sought or Pre-Solicitation notice. It signals intent without commitment. A Contract Notice (F17) is the active competition announcement. A Contract Award Notice (F18) is the obligation record. Just as I cross-reference a U.S. RFI against the award history behind it to understand whether the government has actually funded and executed in this space before, I cross-reference a TED F17 against the F18 history for the same CPV code and awarding authority to understand whether this is a program that produces real contracts or a market research exercise.

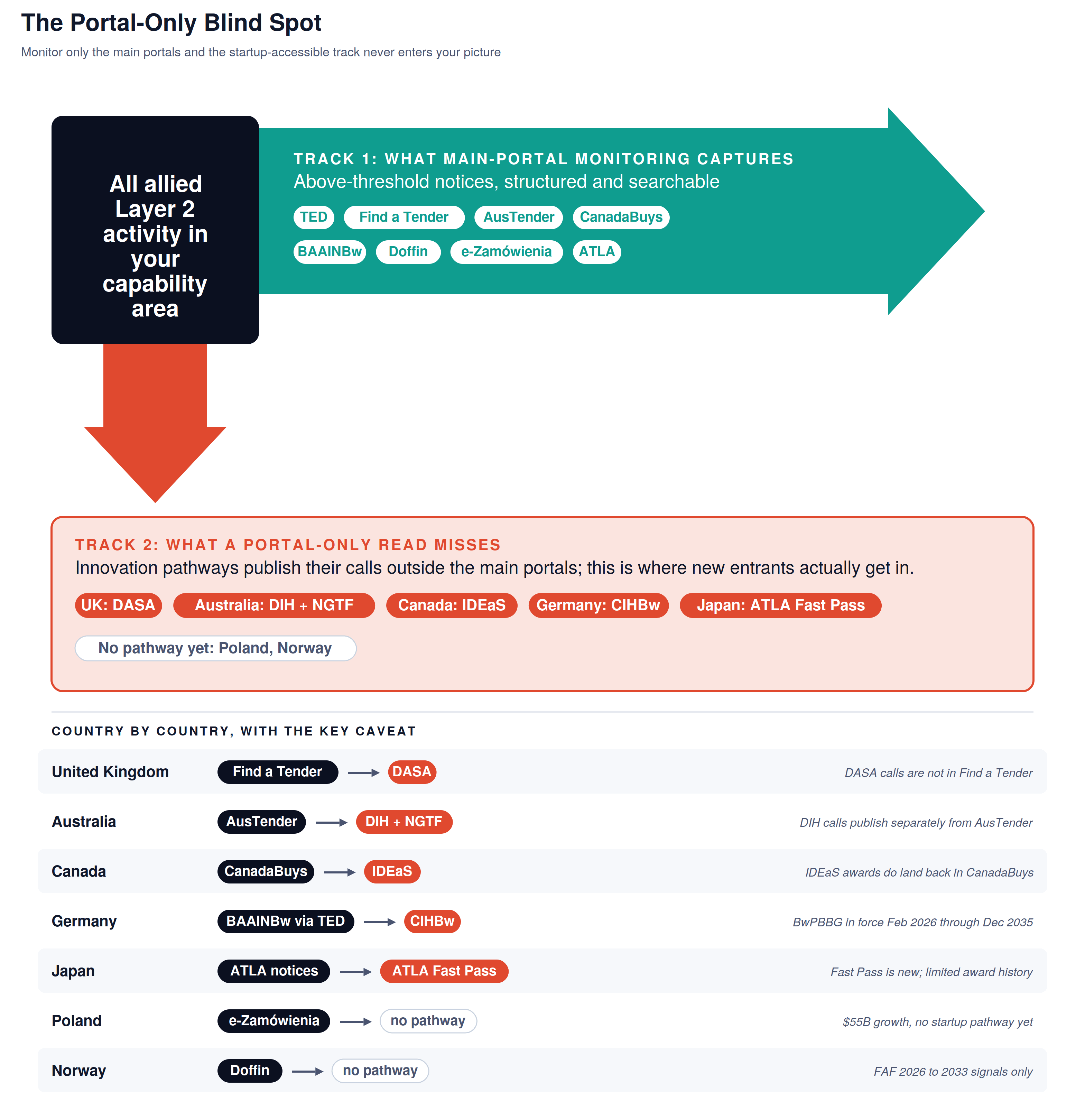

In international Layer 2, the non-traditional pathway gap is identical to the U.S. system: innovation pathway activity does not appear in the main procurement portal. Germany’s Cyber Innovation Hub, the UK’s Defence and Security Accelerator, Australia’s Defence Innovation Hub, Canada’s IDEaS program, and Japan’s ATLA Fast Pass scheme all issue calls for capability that never appear in TED, Find a Tender, AusTender, or CanadaBuys. A team that monitors only the main portal in any of these countries is reading the same incomplete picture as a U.S. team that reads only SAM.gov and misses DIU, AFWERX, and xTechSearch entirely.

Why This Matters

In the U.S. market, a meaningful portion of accessible procurement volume in many capability areas flows through DIU, AFWERX, SOFWERX, and xTechSearch rather than SAM.gov alone. The same dynamic exists in allied markets. DASA themed competitions, Australian DIH investment calls, Canadian IDEaS challenges, and the new Japanese ATLA Fast Pass scheme are where non-traditional procurement activity lives. They require direct portal monitoring separate from the main procurement journal, the same discipline as monitoring U.S. innovation portals separately from SAM.gov.

Ways To Apply This

Build a parallel monitoring set for each target market. For UK: Find a Tender filtered by CPV code plus the DASA open calls page. For Australia: tenders.gov.au plus the Defence Innovation Hub investment themes page. For Canada: CanadaBuys plus the IDEaS challenge cycle page. For EU nations: TED filtered by country and CPV code plus each nation’s national innovation portal. Tag every notice by type before entering it into a pursuit log. A DASA themed competition is not the same signal as a Find a Tender contract notice, and reading them as equivalent produces the same gaps as treating a U.S. Sources Sought and an RFP as identical stages.

Reading the Budget Signal in Allied Markets

The budget layer is the highest-value layer in any defense market, domestic or international, and the one that creates the most positioning runway when read early. In international markets, that tendency to skip it is compounded by an assumption that foreign budget documents are inaccessible, untranslated, or too structurally different from U.S. formats to be actionable. That assumption is partly true for some markets and substantially wrong for others.

For the UK, Australia, and Canada, budget documentation is in English, published publicly, and structured in ways that allow year-over-year trajectory analysis directly analogous to what I run on U.S. R-2 and P-40 exhibits. The UK MoD publishes Main Supply Estimates and an Annual Report that breaks spending by category and capability. Australia’s Portfolio Budget Statements, available at the official Defence budget page (defence.gov.au/about/accessing-information/budgets), go to program-level detail. Canada’s National Defence chapter within Treasury Board Supplementary Estimates follows a comparable format. For EU member states, Germany’s Einzelplan 14, France’s LPM, and Norway’s Future Acquisitions for the Defence Sector (FAF) 2026 to 2033 plan are all publicly accessible.

At the macro level, the SIPRI Military Expenditure Database is the broadest Layer 3 source available. It provides consistent time series on military spending for 170+ countries from 1949 through 2025, freely downloadable. The SIPRI 2025 data reflects 2025 full-year spending, which as of mid-2026 is the most recently published complete annual aggregate. Budget signals precede solicitation activity by 12 to 24 months in most allied systems.

Sourcing note on budget figures below: Figures marked (Primary) trace to official government documents. Figures marked (Media) trace to named defense media and are included because the primary budget documents are in a foreign language or the official English-language summary is not yet published. Both types are cited by source.

Why This Matters

Germany’s BwPBBG is enacted law. Poland’s $55 billion defense budget is an adopted fiscal year figure. Australia’s AUKUS commitment appears in portfolio budget statements. Norway’s FAF 2026 to 2033 plan names specific materiel investment categories. These are Layer 3 signals with the same evidentiary weight as a U.S. P-40 exhibit showing a new-start program element. A team that reads these signals 12 to 24 months before a solicitation appears has positioning runway the public tender record alone cannot provide.

Ways To Apply This

Start at the SIPRI Military Expenditure Database for macro-level trajectory data by country and year. Then go to the primary budget document for each target nation and apply the same reading discipline as a U.S. P-40 or R-2 exhibit: find the program elements in your capability area, document the year-over-year dollar trajectory, note the effort status (new start, continuing, scaling, or declining), and capture the exact justification language. For the UK, that means the MoD Departmental Resources and Main Supply Estimates. For Australia, the Portfolio Budget Statements. For Norway, the FAF 2026 to 2033 plan. For Germany, Einzelplan 14. The program element language in these documents is the same forward-positioning signal as a U.S. comptroller justification book, and it is publicly available.

The Combined Operating Picture

The three layers operate together for international markets the same way they do for U.S. markets. Each answers a different question. No single layer substitutes for the others.

What the Data Cannot Tell You on Its Own

There is a layer that sits beneath all three, and it is worth naming before any of the procurement analysis translates into pursuit planning: market access eligibility. In the U.S. system, this maps to questions about set-aside status, FOCI (Foreign Ownership, Control, or Influence), facility security clearances, and small business certifications. In international defense markets, the equivalent questions involve treaty frameworks, industrial participation requirements, export control regimes, and two additional mechanisms: Foreign Military Sales (FMS) and the NATO Support and Procurement Agency (NSPA).

These are the structural factors that determine whether intelligence translates into a viable pursuit, and they are worth identifying in parallel with the three-layer analysis rather than after it. This is not legal advice. These are reference points for where to start the research.

Foreign Military Sales and Foreign Military Financing

FMS (Foreign Military Sales) is a government-to-government procurement program authorized by the Arms Export Control Act (AECA) and administered within DoD by the Defense Security Cooperation Agency (DSCA). Under FMS, the U.S. government acts as the intermediary: a foreign government submits a Letter of Request (LOR), the U.S. government responds with a Letter of Offer and Acceptance (LOA), and the resulting contract is between the U.S. government and the U.S. contractor, not between the contractor and the foreign government directly. Foreign Military Financing (FMF) is the grant assistance program that funds FMS purchases for eligible countries. For U.S. defense companies, FMS is a significant international revenue pathway that does not appear in any foreign procurement portal. It runs entirely through U.S. government contracting mechanisms and is visible via DSCA notifications, congressional notifications, and SAM.gov contract awards, not through TED, AusTender, or any allied national portal. Understanding whether a foreign capability requirement is likely to be satisfied via FMS, direct commercial sale (DCS), or host-nation procurement is a structural question that belongs at the top of any international market entry analysis.

NATO Support and Procurement Agency (NSPA)

The NSPA (nspa.nato.int) is NATO’s lead organization for multinational acquisition, support, and sustainment, established in 1958 and headquartered in Luxembourg. It manages collective procurement for NATO members and partners across logistics, systems support, fuel, and major equipment programs. NSPA procurements are separate from all national procurement portals. A contract awarded through NSPA does not appear in TED, Find a Tender, AusTender, or any national system. NSPA publishes its own tender notices at nspa.nato.int, and registration in the NSPA Supplier Database is required to participate. For companies targeting NATO collective procurement programs (multi-nation sustainment contracts, alliance-wide capability programs), NSPA is the procurement authority to monitor directly, parallel to but separate from national portal monitoring.

These are the structural factors that determine whether intelligence translates into a viable pursuit. A company that identifies a Polish defense procurement opportunity, for example, needs to understand whether the contract is likely to run through the G2G track (not publicly accessible), the MON-internal procedure track, or the public procurement law track (visible in e-Zamówienia). That determination belongs at the start of the Layer 2 analysis, not after it.

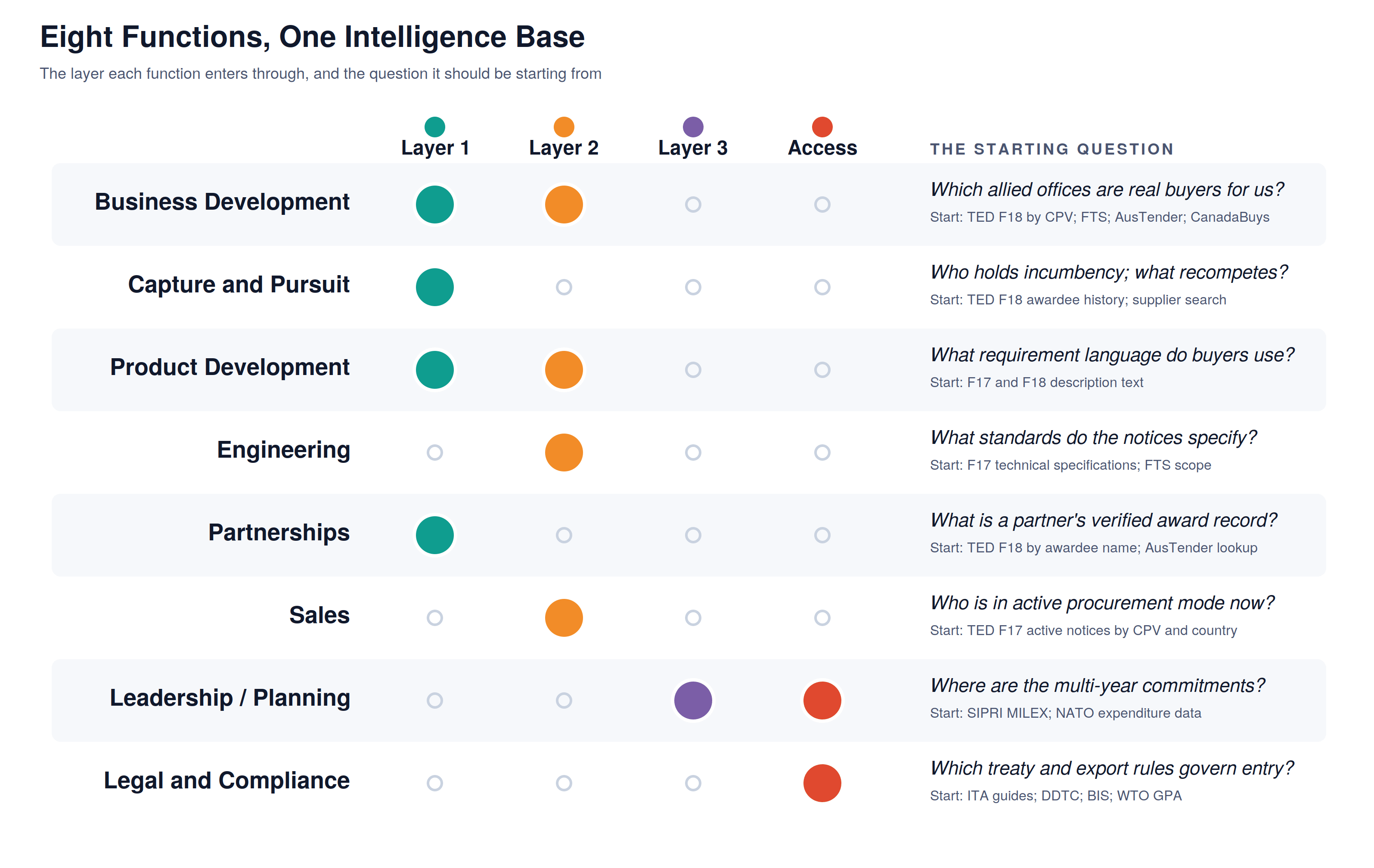

Cross-Functional Applications for International Efforts

Five Patterns Worth Watching in International Defense Market Intelligence

These are patterns I have worked through myself when applying the three-layer process to international markets. Each starts from a real signal. The issue in each case is reading that signal without the surrounding context the other layers provide.

What This Report Does Not Cover

I want to be explicit about three things this report does not address, because they matter for how to use it.

First, it does not cover market access rules in any depth. FMS, NSPA, ITAR, EAR, treaty frameworks, industrial participation requirements, and FOCI considerations for allied market entry are structural factors that precede any BD activity in international defense markets. The access layer table above names the key frameworks and directs you to the right primary sources, but this is not a legal analysis. That analysis belongs with people who practice in this area.

Second, several significant allied defense markets are not covered in detail: Israel, Taiwan, and the Gulf Cooperation Council states. Israel is briefly noted in the data availability matrix but is not analyzed because IMOD/DPD does not publish a structured contract award database comparable to what exists in the Five Eyes or EU systems. Taiwan’s Government e-Procurement System (GEPS) exists and is publicly accessible, but defense-sensitive procurement is substantially exempted. The GCC states operate through direct allocation and royal decrees rather than transparent procurement portals. The focus on the countries where the public data infrastructure is rich enough to support three-layer analysis.

Third, the budget signals documented here are as of June 2026. The SIPRI 2025 data reflects full-year 2025 spending, which is the most recently published complete annual aggregate as of mid-2026. Programs restructure. Budgets get amended. The framework is durable. The specific signals require ongoing monitoring.

Closing Thoughts

If you are in leadership trying to decide whether international defense markets warrant serious attention, the Layer 3 table gives you the starting point. The budget numbers there are not projections. They are enacted or approved spending floors in some of the world’s largest allied defense markets, and several of them include forward acquisition plans that name specific capability investment areas.

If you are in BD or capture and building a pipeline, start with source identification. Build the portal registry by country. Run the Layer 1 award history query for your CPV code in the two or three markets you are most interested in. Look at who the incumbents are, which pathways they used, and when those contracts expire. Add the recompete calendar discipline from that data before looking at anything else. That exercise will tell you more about the competitive structure of an allied market than any trade show conversation.

If you are evaluating a teaming partnership with an allied company, run the award history layer on that company by name across TED, AusTender, Find a Tender, and CanadaBuys as applicable. The public record will show you their actual government footprint, not their self-reported narrative.

Country-specific editions of this framework, applied to individual allied markets, will follow.

Building This Playbook Together

If you are working inside a specific allied defense market and have context the public record does not show, I want to know. Same goes for a source I missed, a figure that conflicts with something I cited, or a program angle I did not cover. This analysis sharpens with input from people working inside these programs and supply chains, and the newsletter is better when the community contributes to it.

Connect with me:

in

STARTUP DoD is an independent newsletter for founders, operators, investors, and teams building in the national security space. All analysis is based on publicly available sources. Nothing in this newsletter constitutes legal, financial, or acquisition advice. This edition is based on publicly available information as of June 2026.

An update to FILE 30: my foreign budgets analysis.

After it ran, an industry friend, Ties Klinkhamer at Keen Venture Partners, kindly pushed back on it & helped me tremendously. His read was simple: the framework tells you where the allied money is. It doesn’t tell you whether you can reach it.

He was right. The budget data is public and runs deep. The path to it isn’t. Companies sit at TRL 5 to 6 with funding in place and government interest confirmed, and still have no route to operational adoption.

So I added the part that was missing.

A pre-filter, before the framework points anywhere: the TRL the pathway requires, whether the market is open or protected, and whether you enter directly or through a prime or consortium.

NATO DIANA, as its own layer above the national portals.

A post-filter, for the TRL 7 to 9 wall where innovation funding ends and operational procurement has not started.

The following maps the full framework, with the additions marked. The complete breakdown is here: shorturl.at/K75Oy

Thank you for the feedback and support all!

Ross